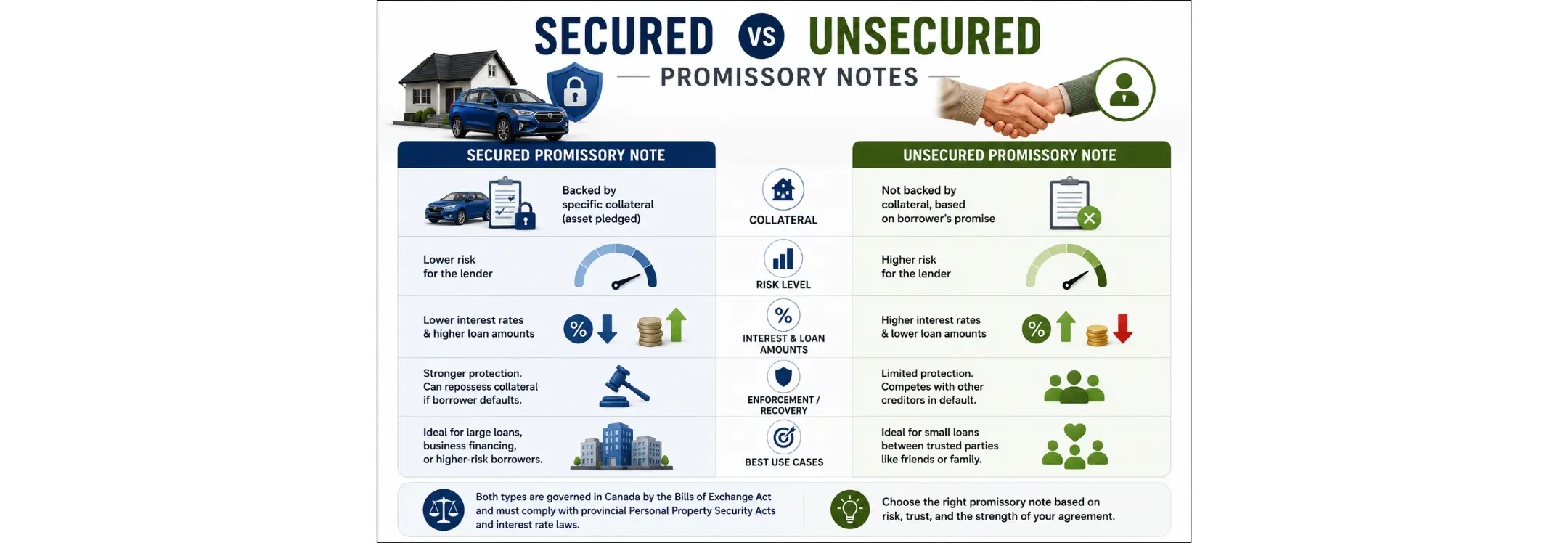

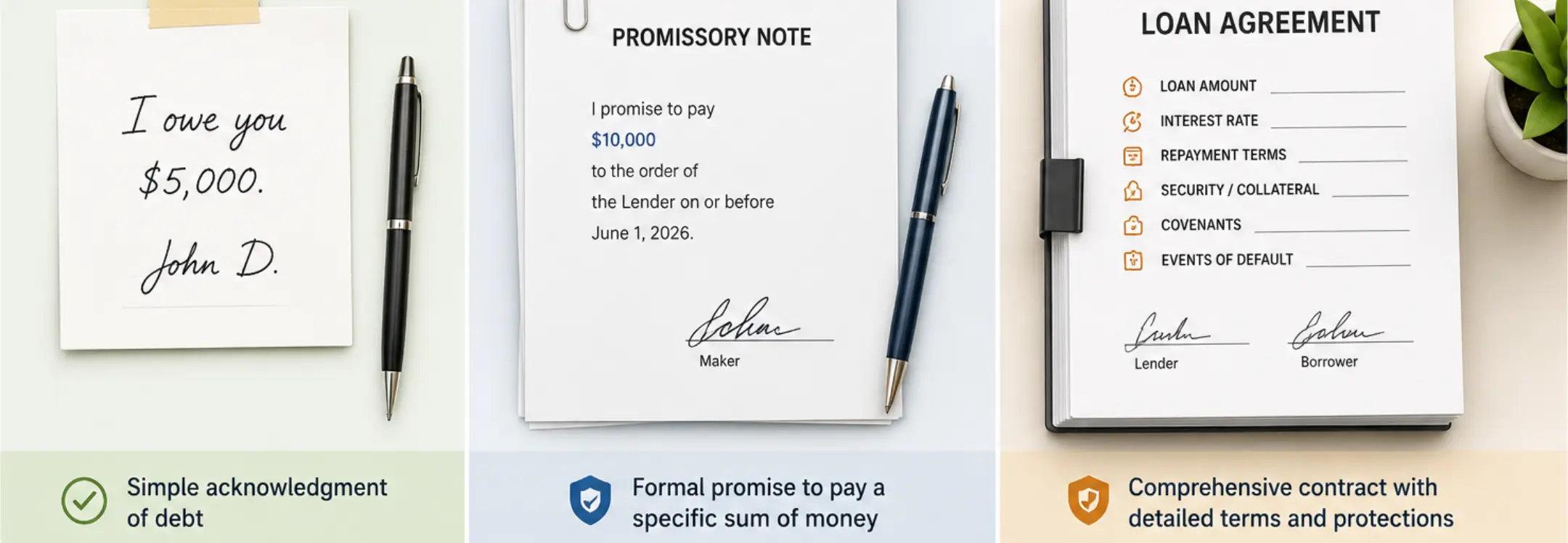

TL;DR- Secured promissory notes require the borrower to pledge specific assets as collateral to guarantee the repayment of the debt.

- Unsecured promissory notes rely entirely on the creditworthiness and the personal or business reputation of the borrower.

- The Bills of Exchange Act is the primary federal legislation that governs the validity and the transferability of promissory notes across Canada.

- As of January 2025 the Criminal Code of Canada sets a maximum interest rate of 35 percent annual percentage rate for most lending agreements.

- Personal Property Security Acts in each province provide the legal framework for lenders to register their interest in collateral and establish priority.

- Secured notes typically offer lower interest rates and higher loan amounts due to the reduced risk for the lender.

- Unsecured notes are often faster to execute and better suited for small loans between trusted parties such as friends or family members.

- You can use Ziji Legal Forms' Templates to easily create a Promissory Note

Introduction: Choosing the Right Promissory Note Type

Lending and borrowing money in the Canadian financial landscape requires a clear understanding of the legal instruments that document these transactions. A Promissory Note Canada is a powerful tool that creates a legally binding commitment to repay a debt. The federal government regulates these instruments through the Bills of Exchange Act which ensures consistency in how debts are acknowledged and transferred across the country. Choosing the right type of Promissory Note depends on the level of risk the lender is willing to accept and the assets the borrower has available to pledge.

The decision to use a secured vs unsecured promissory note is often determined by the size of the loan and the nature of the relationship between the parties. A secured note provides the lender with a safety net by linking the debt to a specific asset like a vehicle or equipment. In contrast an unsecured note is based purely on trust and the financial standing of the maker. Both forms are enforceable in a Canadian court of law provided they contain the essential elements required by federal and provincial statutes.

Understanding the nuances of Canadian law is particularly important because the regulatory environment is currently undergoing significant changes. The recent amendments to the Criminal Code have introduced stricter limits on interest rates to prevent predatory lending practices. Furthermore provincial laws such as the Personal Property Security Act dictate how security interests must be registered to remain valid against other creditors. Selecting the correct instrument ensures that both the lender and the borrower are protected under these evolving legal standards.

The Role of the Bills of Exchange Act

The foundational law for any Promissory Note in Canada is the Bills of Exchange Act which has been in place for decades to provide commercial certainty. This act defines a promissory note as an unconditional promise in writing made by one person to another. It requires the maker to sign the document and engage to pay a sum certain in money on demand or at a fixed future time. This federal oversight means that a note created in one province is generally recognized and enforceable in another.

Significance of the Unconditional Promise

A key requirement for a valid note is that the promise to pay must be unconditional. If the payment is dependent on a contingency or an event that might not happen the document may not qualify as a promissory note under the federal act. This distinction is critical for lenders who want to ensure their document is a negotiable instrument that can be transferred or sold to others. An unconditional promise provides the clarity needed for legal enforcement without the need for complex evidence regarding external conditions.

What Is a Secured Promissory Note

A secured promissory note is a specific type of debt instrument where the borrower grants the lender a security interest in a particular asset. This asset is known as collateral and it serves as a guarantee that the loan will be repaid according to the agreed terms. In Canada the creation of this security interest is governed by the Personal Property Security Act which exists in every province except Quebec. In Quebec similar concepts are handled through the Civil Code using a mechanism known as a hypothec.

The primary purpose of a secured note is to mitigate the financial risk for the person or business providing the funds. If the borrower defaults on their payments the lender has the legal right to seize the collateral and sell it to recover the outstanding balance. This direct access to an asset makes secured notes highly attractive for high value transactions or for lenders dealing with borrowers who have a limited credit history. It provides a physical layer of protection that goes beyond a mere signature on a page.

For a secured note to be fully effective the lender must follow a process known as perfection. This usually involves registering a financing statement in the provincial personal property registry to notify the public of the lender's claim. Registration is vital because it establishes the lender's priority in case the borrower has multiple creditors or files for bankruptcy. Without a perfected interest the lender may find themselves at the end of the line if the borrower's assets are liquidated.

The Mechanism of Security Interest

A security interest is more than just a mention of an asset in a contract. It is a legal right that attaches to the property as soon as the agreement is signed and value is given. Under the provincial Personal Property Security Act the agreement must clearly describe the collateral so it can be identified by third parties. This mechanism ensures that the lender has a proprietary interest in the asset which remains even if the borrower tries to sell the property to someone else without permission.

Role of Personal Property Security Acts

The Personal Property Security Act or PPSA provides a centralized system for managing these financial claims. It replaces older and more fragmented laws that dealt with things like chattel mortgages and conditional sales. By standardizing the rules for how security interests are created and enforced the PPSA makes it easier for lenders to participate in the Canadian market. It offers a predictable framework where priority is generally determined by who registered their interest first in the system.

Importance of Perfection for Lenders

Perfection is the stage where the lender's interest becomes enforceable against third parties like other lenders or a trustee in bankruptcy. While a note might be valid between the borrower and the lender it is not perfected until it is registered or the lender takes physical possession of the collateral. Lenders are encouraged to register their financing statements as early as possible to secure their place in the priority line. In the Canadian legal system the first to register usually has the best claim to the assets if a default occurs.

How Collateral Reduces Lender Risk

Collateral fundamentally changes the risk profile of a loan by providing an alternative source of repayment. Instead of relying solely on the borrower's future cash flow the lender has a claim to an asset with existing market value. This reduces the danger of a total loss if the borrower's business fails or their personal finances collapse. Because the lender has a clear path to recovery they are often more willing to provide funding for projects that might otherwise be considered too risky.

The psychological impact of collateral on the borrower cannot be overstated. When a person knows their vehicle or their business equipment is at stake they are much more likely to prioritize their loan payments. The risk of losing a necessary asset creates a strong incentive for the borrower to remain in compliance with the terms of the Promissory Note. This alignment of interests helps to foster a more stable lending relationship and reduces the likelihood of a contentious default process.

From a legal perspective collateral also simplifies the recovery process. In many Canadian provinces a secured lender can repossess collateral without going to court first as long as they can do so peacefully. This is a much faster and cheaper option than filing a lawsuit and waiting for a judge to issue a judgment. The ability to quickly liquidate an asset ensures that the lender can recoup their funds while the asset still holds its value which is particularly important for items like electronics or vehicles that depreciate over time.

Enhancing Loan Recoverability

Recoverability refers to the ease with which a lender can get their money back after a borrower stops paying. Collateral enhances this by creating a specific pool of value that is dedicated to the debt. Even in a crowded bankruptcy scenario the secured creditor has the right to the proceeds from their specific collateral before anyone else gets paid. This structural advantage is the reason why secured lending is the preferred method for major financial institutions and professional private lenders across Canada.

Deterrence of Fraudulent Transfers

Another layer of risk reduction comes from the PPSA registry itself. Because the security interest is public record it is much harder for a dishonest borrower to sell the collateral and disappear with the cash. Any savvy buyer in Canada will perform a PPSA search before purchasing high value items like cars or machinery. If the search reveals an existing lien the buyer will know that the lender still has a claim to the property. This transparency protects the lender's interest from being diluted by unauthorized sales.

Common Collateral Types

In the Canadian market the types of collateral used in a secured note are diverse and depend on the borrower's situation. For personal loans motor vehicles are the most frequent choice because they are easy to identify and have a well established resale market. Vehicles are registered using their unique Identification Numbers which makes them simple to track in provincial registries. Other common personal assets include jewelry and high end electronics or even recreational equipment like boats and motorcycles.

Business borrowers often pledge assets that are essential to their operations to secure a Promissory Note template. This can include specialized machinery and office equipment or furniture and fixtures. Some businesses may even pledge their inventory or their accounts receivable which are the amounts owed to them by their own customers. While these are considered more fluid assets they can be very valuable for companies that do not own significant real estate or heavy equipment.

Intangible assets are also becoming more common as security in the modern economy. A borrower might pledge their intellectual property such as trademarks or patents or even their shares in a private corporation. While these require more complex valuation and documentation they provide a way for tech startups and creative firms to access secured funding. Regardless of the type of asset it is crucial that the Promissory Note Canada includes a clear and accurate description to ensure the security interest is enforceable.

Real Property as Collateral

While many promissory notes are secured by personal property some also involve real estate. If a lender wants to use land or buildings as security they will typically require a mortgage or a deed of trust in addition to the note. Real estate is often considered the most stable form of collateral because it generally appreciates over time and cannot be easily moved or hidden. However the legal process for foreclosing on real property is more regulated and time consuming than repossessing a vehicle.

Investment and Financial Assets

For sophisticated lending arrangements borrowers may use financial instruments as collateral. This can include mutual funds or guaranteed investment certificates and other securities. These assets are particularly attractive to lenders because they can be liquidated almost instantly if a default occurs. Lenders often gain "control" over these accounts to ensure the borrower cannot withdraw the funds without the lender's knowledge. This provides a high level of security that is equivalent to holding cash.

Benefits for Borrowers

It is a common misconception that secured notes only benefit the lender. In reality a borrower can gain significant financial advantages by offering collateral. The most immediate benefit is a lower interest rate. Because the lender is taking on less risk they do not need to charge as high of a premium for the loan. Over a period of several years the savings on interest can amount to a substantial sum of money which the borrower can use for other needs.

Secured notes also open the door to larger loan amounts and longer repayment terms. A lender who might only lend a few thousand dollars on an unsecured basis may be willing to lend tens of thousands if a vehicle or equipment is involved. The longer repayment period means that the monthly installments are smaller and more manageable. This improved cash flow can be the difference between a small business growing or stagnating during its first few years of operation.

For those with poor credit or a limited financial history a secured note provides a path to credit rehabilitation. By successfully managing a secured loan the borrower demonstrates to the financial community that they are responsible and reliable. Many lenders report these payments to credit bureaus which helps the borrower build a positive score over time. This can eventually lead to the borrower qualifying for traditional bank loans and lower interest rates on other forms of credit.

Improved Approval Odds

Secured loans are generally easier to obtain than unsecured ones especially when the economy is uncertain. Lenders are more likely to approve an application when they know they have a fallback option. This is particularly helpful for self employed individuals or new entrepreneurs who may not have the steady income history that banks typically look for. By using their existing assets they can provide the assurance a lender needs to say yes to their request for funding.

Access to Specialized Financing

Some types of financing are only available on a secured basis. For example many vendors will only offer terms if the goods being sold serve as security for the debt. This is common in the construction and manufacturing industries where the equipment being purchased is high value. By agreeing to a secured note the borrower can acquire the tools they need to complete jobs and generate revenue without having to pay the full cost upfront. It is a strategic way to leverage assets for business growth.

What Is an Unsecured Promissory Note

An unsecured promissory note is a legal document where the borrower promises to repay a debt without pledging any specific assets as collateral. In this arrangement the lender is essentially relying on a handshake in written form. There is no property for the lender to seize immediately if the borrower stops making payments. Instead the lender must use the court system to try and collect the money which can be a long and expensive process. These notes are often used for smaller amounts or when the parties have a high degree of mutual trust.

In the world of Canadian law an unsecured note is still a binding contract that falls under the Bills of Exchange Act. If a borrower fails to honor the note the lender can sue them for a breach of contract. If the lender wins they will receive a court judgment which they can then use to garnish wages or freeze bank accounts. However since there is no specific asset linked to the loan the lender has no priority over other creditors. If the borrower goes bankrupt the unsecured lender is often left with nothing.

Despite the higher risk for lenders unsecured promissory notes are very popular because of their simplicity and speed. There is no need to hire an appraiser to value collateral or to file complex registrations with the provincial government. For a small loan between family members or for a quick business bridge loan an unsecured note is often the most practical choice. It records the debt and the interest rate without the administrative burden that comes with a secured transaction.

The General Creditor Status

When a lender holds an unsecured note they are considered a general creditor in the Canadian legal system. This means they have a claim against all of the borrower's non exempt assets rather than one specific item. While this sounds broad it is actually a weaker position because other creditors may have already claimed the most valuable assets through secured notes or mortgages. In a situation where a borrower has more debt than assets the general creditors are usually the last to receive any payment from a liquidation.

Unsecured Notes as Negotiable Instruments

Like their secured counterparts unsecured notes can be negotiable instruments. This means that the lender can sell the note to a third party or a debt collector for a cash payment today. However because there is no collateral the market value of an unsecured note is generally lower. A buyer will only be interested if the borrower has a very strong credit rating and a clear ability to pay. The transfer of an unsecured note still requires a proper endorsement and delivery to the new holder.

Reliance on Borrower Credibility

In the absence of collateral the credibility of the borrower is the only thing that matters to a lender. This credibility is typically measured by the borrower's credit score and their history of managing past debts. In Canada a credit score is a numerical snapshot of a person's financial reliability as reported by agencies like Equifax and TransUnion. A lender will also look at the borrower's steady income and their current debt to income ratio to ensure they can afford the new payments.

Personal reputation and professional history also play a massive role in unsecured lending. In small communities or specialized industries a person's word is their most valuable asset. If a borrower has a long history of successful business ventures and honest dealings a lender may be happy to provide an unsecured loan. This "character based" lending is the foundation of many informal agreements between colleagues and family members where the relationship itself serves as a form of security.

However even with a credible borrower things can go wrong. A sudden job loss or a medical emergency or a business downturn can leave even the most honest borrower unable to meet their obligations. This is why lenders should always perform their due diligence before agreeing to an unsecured note. It is not enough to like the borrower; you must be convinced that they have the financial stamina to handle the debt even if their situation changes for the worse over the life of the loan.

Evaluating the Ability to Pay

Lenders often request proof of income such as pay stubs or tax returns before issuing an unsecured note. This allows them to verify that the borrower is not overextending themselves. In the Canadian context the stability of the borrower's employment is also a key factor. A borrower who has been with the same employer for ten years is generally seen as a much lower risk than someone who changes jobs every few months. This "capacity" to pay is the bedrock of any successful unsecured lending arrangement.

Psychological Trust in Informal Lending

In loans between friends and family the trust is often more emotional than financial. The lender believes in the borrower's dreams or wants to help them through a difficult time. While this is admirable it can lead to problems if the terms are not written down clearly. Using an Online Promissory Note provides a professional boundary that helps protect the relationship. It ensures that both parties view the transaction as a serious financial obligation rather than a gift which can prevent years of resentment if the borrower is slow to pay back the funds.

Typical Use Cases

Unsecured promissory notes are the workhorse of small scale and short term financing in Canada. One of the most common use cases is for personal loans between friends or relatives. Whether it is helping a cousin with a down payment or lending a friend money for car repairs these situations rarely involve collateral. The amounts are usually low enough that the parties do not want the hassle of a formal security agreement but they still want a legal record to prevent any future confusion.

Another frequent use case is in the early stages of a business startup. Early stage private investors often provide seed money through unsecured notes that can later convert into company shares. Since a brand new company may have no physical assets to pledge the investor is betting on the founders and their vision. These notes are a flexible way for businesses to get off the ground without the restrictive requirements of a traditional bank loan. They provide the "runway" a new company needs to build a product and find customers.

Unsecured notes are also used for "bridge financing" in both personal and business contexts. This is a short term loan designed to cover expenses until a larger sum of money becomes available. For example a business might use an unsecured note to pay its employees while it waits for a large customer payment to arrive. A person might use one to cover the gap between buying a new house and selling their old one. In these scenarios the speed and simplicity of an unsecured note are the primary advantages.

Student and Educational Loans

Many educational institutions and private lenders provide student loans using unsecured promissory notes. These are based on the student's future earning potential rather than their current assets. Because a student may not own a home or a car an unsecured note is the only way for them to access the funds needed for tuition and living expenses. These notes often have specialized terms such as grace periods where the student does not have to make payments until they graduate and find a job.

Corporate Commercial Paper

Large corporations with very high credit ratings often issue unsecured notes known as commercial paper to investors. This allows them to borrow millions of dollars for a few days or months at very low interest rates. For these companies the reputation of the firm is so strong that investors do not feel the need for collateral. While this is a more sophisticated version of the promissory note it follows the same basic legal principles of an unconditional promise to pay a sum certain.

Risk Profile for Lenders

The risk profile for an unsecured lender is significantly higher than for a secured one. The most obvious danger is the "disappearing borrower" or the "judgment proof" debtor. If a borrower has no assets and no job a court judgment is just a piece of paper with no real value. The lender may spend thousands of dollars on legal fees only to find that there is nothing to collect. This is why unsecured notes should generally be reserved for smaller amounts that the lender can afford to lose if the worst happens.

In a bankruptcy or insolvency situation unsecured lenders are at a major disadvantage. Canadian law prioritizes secured creditors and certain government claims before anything is paid to general creditors. By the time the mortgage holders and the car lenders are paid off there is rarely enough money left to satisfy the unsecured notes. This "all or nothing" nature of unsecured lending means that a single default can have a much larger impact on a lender's overall portfolio than a default on a secured loan.

To manage this risk lenders must be careful about the interest rate they charge. While a higher rate provides a bigger return it also increases the borrower's monthly burden which can actually make a default more likely. Lenders must also stay within the criminal interest rate limits which were reduced to 35 percent APR in early 2025. Charging a rate above this limit is a criminal offense and will likely make the entire Promissory Note Canada unenforceable in court.

The Danger of Competing Creditors

An unsecured lender has no way to prevent the borrower from taking out more debt after the note is signed. If the borrower gets into financial trouble they might stop paying the unsecured note while they continue to pay their car loan or their credit cards. Since the car lender can take the car they have more leverage over the borrower. The unsecured lender is often the first one to be ignored when money gets tight which highlights the importance of keeping a close eye on the borrower's financial health.

Costs of Legal Enforcement

Suing a borrower for non payment is not a free process. In Canada a lender must pay filing fees and potentially hire a process server or a lawyer or a paralegal. Even in Small Claims Court these costs can add up quickly. If the loan is only for a few hundred dollars it may not be worth the time and expense to pursue it through the legal system. This "enforcement gap" is a major risk for unsecured lenders and it is why many choose to use debt collection agencies instead of taking the matter to court themselves.

Key Differences Between Secured and Unsecured Notes

The most fundamental difference between a secured and an unsecured note is the presence of a "safety net" for the lender. A secured note is tied to a specific piece of property while an unsecured note is tied only to the borrower's personal promise. This one distinction creates a domino effect that influences every other term of the loan including the interest rate and the repayment schedule and the consequences of a missed payment. Understanding these differences is the key to choosing the right Promissory Note Canada for your specific needs.

In the Canadian legal system a secured note gives the lender "proprietary rights" which means they have an interest in the asset itself. An unsecured note only gives the lender "contractual rights" which means they have a right to be paid but no specific claim to any of the borrower's things. If the borrower tries to sell a secured car the lender's lien stays on the title until the loan is paid off. If the borrower sells a television that was bought with an unsecured loan the lender has no way to stop the sale or get the television back from the new owner.

From an administrative standpoint secured notes require significantly more work. You must accurately describe the collateral and perform a search to make sure no one else has a claim to it and then register your own claim with the province. Unsecured notes are much simpler and can be completed by just filling in the names and the payment dates. This trade off between safety and simplicity is the most important factor for any lender to consider before they hand over their money.

Comparison of Priority in Bankruptcy

One of the most critical differences appears during a bankruptcy proceeding. In Canada the Bankruptcy and Insolvency Act provides a strict hierarchy for who gets paid first. Secured creditors are at the top of the list because they already have a legal claim to a specific asset. They can often just take their collateral and sell it regardless of what the other creditors want. Unsecured lenders are much further down the list and must wait to see if there is any money left after the secured parties and the government are satisfied.

Impact on the Borrower's Credit Report

While both types of notes can affect a borrower's credit score they do so in different ways. A secured note is often seen by other lenders as a more stable and responsible form of debt. It shows that the borrower was able to provide collateral and is successfully managing a complex financial arrangement. An unsecured note may be seen as more of a "last resort" if the borrower has a lot of them. However as long as the payments are made on time both types of notes will help the borrower build a positive credit history in Canada.

Collateral Backing

Collateral is the anchor of a secured note. It must be something of value that the borrower owns and has the right to pledge. In Canada the collateral is typically personal property like a vehicle or equipment or even financial instruments like stocks and bonds. The note must include a detailed description of the collateral including serial numbers or Identification Numbers to ensure it can be easily identified by a court or a bailiff. This link between the debt and the asset is what gives the lender their power in the transaction.

In an unsecured note there is zero collateral backing. The lender cannot point to any specific thing the borrower owns and say "that is mine if you don't pay." This lack of an anchor is why unsecured notes carry such a high risk. The lender is essentially gambling that the borrower will remain employed and honest for the entire duration of the loan. If the borrower loses their job the lender has no physical asset to fall back on to recover their investment.

This difference also affects the "limit of recovery." For a secured loan the lender can recover up to the value of the collateral plus any costs of seizure and sale. If the collateral is worth more than the debt the lender must return the extra money to the borrower. For an unsecured loan the lender can theoretically recover from any of the borrower's assets but they must compete with everyone else to do so. This makes the "floor" of a secured loan much higher and more predictable than the "ceiling" of an unsecured one.

Verification of Collateral Value

Lenders in a secured transaction should perform an appraisal or use a guide like the Canadian Black Book for vehicles to ensure the collateral is worth enough to cover the loan. If a lender accepts a five thousand dollar car as security for a ten thousand dollar loan they are only truly "secured" for half of the debt. The other half is essentially an unsecured loan. This "loan to value" ratio is a critical calculation for professional lenders and it highlights why picking the right asset is so important.

Protection Against Asset Deterioration

A major challenge for secured lenders is that assets can lose value over time. A car can be crashed and a piece of machinery can break and electronics can become obsolete. This is why many secured promissory notes include a requirement for the borrower to maintain insurance and perform regular maintenance. If the collateral is destroyed the lender wants to make sure the insurance company will pay them the balance of the loan. Unsecured lenders do not have to worry about these details because their claim is against the person rather than the property.

Risk Levels and Protections

The risk levels are the polar opposites of each other. Secured lending is a defensive strategy designed to protect the lender's capital at all costs. It provides multiple layers of protection including the value of the collateral and the priority in the PPSA registry and the right to repossess without a court order. For a lender who is using their retirement savings or who is lending to a stranger a secured note is the only way to sleep soundly at night.

Unsecured lending is an offensive strategy focused on simplicity and potentially higher returns. The lender is taking on a much higher risk of total loss in exchange for a faster process and a higher interest rate. The only real protection for an unsecured lender is a thorough credit check and a solid legal document that can be used in court if necessary. This is a much more aggressive form of lending that requires a high tolerance for uncertainty and the willingness to walk away from the money if the borrower disappears.

Borrowers also have different protections under the law. In several Canadian provinces there are "seize or sue" rules for consumer goods. These rules state that a lender must choose between taking the collateral or suing the borrower but they cannot do both. If the lender seizes consumer goods, they generally lose the right to claim any deficiencies. This protects the consumers from losing their property and still being pursued for the remaining debt. Unsecured borrowers do not receive this protection - unsecured creditors must sue to collect and once they obtain a judgment, they can garnish wages, freeze bank accounts, or seize non exempt assets.

The Role of Limitation Periods

All promissory notes in Canada are subject to limitation periods which are deadlines for starting a lawsuit. In provinces like Ontario and Alberta the general limit is two years from the date the borrower defaulted on their payment. For an unsecured lender this deadline is a ticking clock. If they miss it they lose their only way to collect the money. A secured lender also faces this deadline if they want to sue the borrower but they may still have the right to repossess the collateral even after the limitation period for a lawsuit has passed in some jurisdictions.

Statutory Exemptions from Seizure

Even if an unsecured lender wins a court judgment they cannot take everything the borrower owns. Every Canadian province has an Execution Act that lists certain "exempt" assets that are off limits to creditors. This usually includes basic household furniture and some clothing and the tools the borrower needs for their trade and often a low value vehicle. A secured lender avoids these exemptions because the borrower specifically agreed to give up that property if they defaulted. This makes secured notes much more effective at reaching into a borrower's wealth.

Interest Rate Implications

Interest rates are the "price" of risk in the lending world. Because secured notes are safer for the lender they generally carry lower interest rates. In the current Canadian market a secured private loan might be offered at six or eight percent depending on the quality of the collateral. This makes the loan more affordable for the borrower and reduces the chances that they will default due to high monthly costs. It is a more sustainable form of borrowing for long term needs.

Unsecured notes demand a much higher interest rate to compensate the lender for the possibility of a total loss. It is not uncommon to see unsecured private loans with interest rates of fifteen or twenty percent. However lenders must be extremely careful not to cross the "criminal rate" threshold. As of early 2025 the Criminal Code of Canada sets the limit at an annual percentage rate of 35 percent for most transactions. Charging more than this can lead to prison time and heavy fines for the lender.

The method of interest calculation must also be clearly stated in the note. Under the Interest Act of Canada if a note states a rate for a period less than a year it must also state the equivalent annual rate. If this is missing the lender may be legally limited to an interest rate of only five percent per year regardless of what the note says. This is why using a professional Promissory Note template is so important; it ensures that the interest language meets all federal requirements and is fully collectible.

Fixed vs Variable Interest Rates

Secured notes often use variable interest rates that are tied to a benchmark like the bank prime rate. This protects the lender from inflation over a long loan term. Unsecured notes are more likely to use fixed interest rates because they are shorter in duration and the parties want certainty about the total cost of the loan. In either case the Promissory Note Canada should clearly define how often interest is compounded such as monthly or semi annually. This clarity prevents disputes over the final amount owed when the loan is paid off.

Prepayment Penalties and Fees

Some promissory notes include fees for late payments or penalties if the borrower pays the loan off early. In Canada these must be "reasonable" and cannot be used as a disguised form of interest to bypass the 35 percent criminal rate cap. Secured notes are more likely to include these because the lender has gone through more effort and expense to set up the loan. Unsecured notes often allow for "anytime repayment" without a penalty which is a major advantage for borrowers who expect to get a windfall of cash soon.

Default and Enforcement Options

When a borrower misses a payment on a secured note the lender has a range of powerful options. They can often hire a private bailiff to repossess the car or equipment without any help from the court. Once they have the property they must give the borrower a chance to "redeem" it by paying the full debt. If the borrower cannot pay the lender sells the property at an auction or through a private sale. This is a relatively mechanical process that focuses on the asset rather than the person.

Enforcing an unsecured note is a much more person centered and time consuming process. The lender must first send a formal demand letter to remind the borrower of their debt. If that fails they must start a lawsuit and prove their case in a courtroom. Even after winning they have to play a game of "detective" to find the borrower's assets or their place of employment to start a garnishment. It is a reactive process that depends heavily on the borrower having some form of income or non exempt property to take.

These enforcement differences also impact the cost of the loan for the borrower. Many promissory notes state that the borrower is responsible for all legal and collection costs if they default. Because it is so much more expensive to sue someone than to repossess a car the "default costs" for an unsecured borrower can be much higher than for a secured one. A borrower who owes five thousand dollars on an unsecured note could easily end up owing ten thousand after legal fees and court costs are added to the bill.

The Role of the Sheriff and Bailiff

In Canada enforcement of a court judgment for an unsecured debt is often handled by the Sheriff's office or a court appointed bailiff. These officials have the authority to enter a borrower's premises and seize assets that are listed in a Writ of Seizure and Sale. However they are strictly governed by the law and must respect the exemptions for basic necessities. Secured lenders often use private bailiffs who operate under the terms of the security agreement rather than a court order which gives them more flexibility but also requires them to act reasonably to avoid liability.

Mediation and Alternative Dispute Resolution

Because court cases are so slow many modern promissory notes include a clause requiring the parties to try mediation or arbitration before going to a judge. This is especially common for unsecured notes where the costs of a full trial would be more than the value of the loan. Mediation is a guided conversation where a neutral third party helps the borrower and lender reach a new payment plan. It is often a "win win" because the lender gets some of their money back without a fight and the borrower avoids having a judgment on their permanent record.

Loan Amounts and Terms

Secured notes are the standard for high value transactions in Canada. If you are lending fifty thousand dollars for a business expansion or twenty thousand for a new truck you almost certainly want that debt secured. The security allows for longer loan terms such as three to five years or even longer. This long duration gives the borrower the time they need to use the funds to generate a return while the lender feels safe knowing that their principal is protected by a physical asset.

Unsecured notes are typically reserved for smaller amounts usually under ten thousand dollars. At this level the risk is small enough that a lender may be willing to rely on the borrower's signature. The terms are also much shorter often requiring full repayment within six months or a year. These are designed to be "bridge" solutions rather than long term capital arrangements. A borrower who needs a large sum for a long time will almost always be asked for collateral by any professional lender.

The way the money is paid back also differs. Secured notes are almost always installment loans with a set schedule of monthly or bi weekly payments. This predictability is necessary for the lender to monitor the loan's progress. Unsecured notes are more likely to be "demand notes" or have a single "balloon payment" at the end of the term. This provides more flexibility for the borrower but it also means the lender has to be very confident that the borrower will have the full sum available on the due date.

Acceleration Clauses on Default

A common feature in both types of notes is the "acceleration clause." This says that if a borrower misses a single payment the entire balance of the loan becomes due immediately. This is a vital protection for the lender. Without it a lender might be forced to sue the borrower separately for every single missed payment. In a secured note the acceleration clause is usually the trigger that allows the lender to start the repossession process. In an unsecured note it allows the lender to sue for the full amount of the debt all at once.

Negotiating Terms for Special Situations

Because promissory notes are private contracts the parties have a lot of room to negotiate. A borrower might offer "partial security" where they pledge an asset that is worth less than the full loan to get a slightly better interest rate. Or a lender might agree to an unsecured note but require a higher interest rate and a shorter repayment period. This flexibility is the greatest strength of the Promissory Note Canada. It allows people to craft a financial deal that fits their specific needs and their specific level of trust.

When to Use a Secured Promissory Note

A secured promissory note is the correct tool to use whenever the potential loss from a default would be significant for the lender. It is not just about the money; it is about the "exit strategy" for the loan. If you are lending funds and you cannot afford to wait months for a court case then you need the immediate remedy that collateral provides. In the Canadian financial world a secured note is a sign of professionalism and serious intent. It turns a personal favor into a structured business transaction that is respected by the legal system and other creditors.

Lenders should also insist on security when they are dealing with a borrower who has a fluctuating income or a new business. Even the most honest person cannot pay back a loan if their income disappears. A secured note ensures that the lender is not left with empty hands if the borrower's luck turns. It is also the best choice when the borrower is using the funds to purchase a specific asset. In that case the asset itself can serve as the security which is a fair and logical arrangement for both sides.

For borrowers using a secured note can actually be a sign of strength. It shows that you have valuable assets and that you are willing to stand behind your promise to pay. By offering collateral you are taking an active role in reducing the lender's risk which gives you more leverage to negotiate for lower interest rates and better terms. It is a strategic move that can save you thousands of dollars in borrowing costs over the life of the loan and help you build a much stronger relationship with your financier.

Large Loan Amounts

When a loan amount exceeds the threshold of what a lender can comfortably lose security is a mandatory requirement. In Canada most private lenders start asking for collateral once a loan moves past the five or ten thousand dollar mark. For amounts in the range of twenty thousand to fifty thousand dollars an unsecured note is virtually unheard of outside of extremely close family relationships. At this level the lender's primary concern is "capital preservation" and a secured note is the only way to achieve it.

Large loans also carry a higher risk of being challenged in court or by other creditors. A secured note that is properly registered provides a clear and undeniable record of the debt. It acts as a shield that protects the lender's claim from being ignored or pushed aside by newer creditors. This legal robustness is essential when significant sums of money are at stake. It ensures that the transaction follows the "standard operating procedure" for high value Canadian finance.

Furthermore large loans often have complex repayment schedules that span several years. During that time the borrower's life or business can change in many ways. A secured note provides the lender with a "seat at the table" during these changes. If the borrower tries to sell their business or file for bankruptcy the secured lender is one of the first people who must be dealt with. This ongoing involvement is a key part of managing the risk of a large long term financial commitment.

Business Transactions and Asset Purchases

Secured promissory notes are the lifeblood of small business financing in Canada. When a company buys a new piece of equipment the seller often provides "vendor financing" using a secured note. The equipment being sold serves as the collateral. This is a perfect arrangement because the equipment is what generates the revenue used to pay off the loan. If the business fails the vendor can simply take back the equipment and sell it to someone else which minimizes their loss and allows them to provide funding to more customers.

These notes are also vital during the purchase and sale of an entire business. It is common for a buyer to pay sixty or seventy percent in cash and give the seller a note for the remaining balance. The seller will almost always want that note secured by the assets of the business they are selling. This "seller carry back" financing is a major part of the Canadian economy and it only works because of the protections offered by secured promissory notes and the PPSA registry system.

For a business borrower using a secured note is often the only way to access the capital needed for expansion. Most banks will not lend to a company that does not have at least two or three years of profitable tax returns. A private lender or an equipment vendor using a secured note can be much more flexible. They are looking at the value of the asset rather than the historical profit of the firm. This makes secured notes a critical tool for young and growing companies that need to scale up their operations quickly.

Limited Borrower Credit History

One of the greatest benefits of a secured note is its ability to overcome a poor credit score. In the Canadian credit system once you fall below a certain score traditional banks will simply stop looking at your applications. A private lender using a secured note can be the "lender of last resort" for these individuals. By providing collateral the borrower is saying "don't look at my past mistakes; look at this asset I own right now." It is a powerful way to reboot a financial reputation.

This is also a common scenario for newcomers to Canada who have not yet had time to build a local credit file. They may have been very successful in their home country but that history does not follow them to Canada. By using a secured note to buy a car or start a small business they can establish their first footprints in the Canadian financial system. It allows them to participate in the economy immediately rather than waiting several years for their credit score to catch up with their actual financial capability.

Lenders who provide these "second chance" loans are performing a valuable service but they must protect themselves. A secured note is the only way to do that safely. It ensures that their "act of faith" in the borrower is backed by a tangible asset. If the borrower succeeds the lender gets their interest and the borrower gets a better credit score. If the borrower fails the lender takes the collateral and recoup their principal. It is a balanced approach to high risk lending that benefits both the community and the individual lender.

Lender Protection Preference

Some people are simply more cautious with their money than others. If you have worked hard to save up fifty thousand dollars you have every right to want the maximum possible protection when you lend it out. A secured note is the "gold standard" for lender protection in Canada. It provides a direct path to repayment that does not depend on the borrower's honesty or the speed of the court system. For many private lenders this peace of mind is worth more than the extra effort required to document and register the security.

This preference for protection is especially important in a volatile economy. When interest rates are changing and industries are being disrupted a borrower's income can be very unpredictable. A secured note provides a "hedge" against this uncertainty. Even if the borrower loses their job the car or the equipment still has a value that can be realized in the market. It ensures that the lender is not the one who pays the price for the borrower's bad luck or the country's economic challenges.

Using a secured note also sets a professional tone that can prevent the borrower from taking advantage of the lender. Some people view an unsecured loan from a friend as a low priority debt that they can pay back whenever they feel like it. When a borrower has to sign a security agreement and sees a PPSA registration against their property they realize that this is a serious business deal. This professional boundary is the best way to ensure that the loan is repaid on time and that the friendship or family bond remains intact.

When to Use an Unsecured Promissory Note

An unsecured promissory note is the instrument of choice for "character based" lending where the amount is low and the trust is high. It is a tool for speed and simplicity in the Canadian financial market. You should use an unsecured note when the administrative costs of securing the debt would be more than the value of the safety net itself. In many personal and professional situations a simple written promise is all that is needed to ensure that a debt is recognized and eventually paid back.

These notes are also ideal for situations where the borrower needs a "hand up" and the lender is in a position to take a small risk. For a five hundred dollar loan to a coworker or a thousand dollars to a sibling an unsecured note is the most logical path. It avoids the awkwardness of asking for collateral while still providing the legal structure needed to track the debt. It is a way to be generous and helpful while still being financially responsible.

Lenders should use an unsecured note when they have a long and successful history with the borrower. If you have lent money to a business partner five times before and they have always paid you back with interest then a secured note might be unnecessary "overkill". In these cases the relationship itself is the security. The borrower knows that if they fail to pay they will lose a valuable professional ally which is often a much greater deterrent than the risk of losing a piece of equipment.

Small Personal Loans

In Canada the Small Claims Court is designed to handle disputes over relatively small amounts of money. Because an unsecured note is a straightforward contract it is very easy to enforce in these courts. For a loan of a few thousand dollars the "threat" of a Small Claims case is often enough to keep a borrower honest. The lender does not need the extra power of collateral because the legal system provides a simple and effective way to get a judgment for these smaller debts.

Small loans also tend to have shorter durations. If a loan is only for three or six months the risk of a major change in the borrower's life is much lower. The lender can make a reasonably good guess about the borrower's ability to pay over such a short window. In these "micro lending" scenarios the speed of the transaction is often the most important factor for the borrower and an unsecured note is the fastest way to get the funds into their hands.

Using an unsecured note for small loans also saves the borrower money. There are no registration fees to pay and no need for expensive insurance on collateral. For someone who is already in a tight financial spot these extra costs can be a real burden. An unsecured note provides a "low friction" way to access credit that helps the borrower without adding unnecessary complexity to their life. It is the most "human centered" form of lending.

Strong Personal or Professional Relationships

Trust is the currency of the unsecured promissory note. When two people have worked together for years or have grown up together they have a "social contract" that is more powerful than any PPSA registration. Lending money on an unsecured basis is a way to honor that bond. It shows the borrower that you believe in them and that you value the relationship more than a piece of property. In many Canadian cultures this show of trust is the key to building long term loyalty and mutual support.

In the business world unsecured notes are often used between "strategic partners." If two companies are working on a project together one might lend the other funds to cover a temporary shortfall. Because they are both invested in the success of the project the lender is confident that the borrower will do everything in their power to pay the money back. The note is just a way to keep the books clean and satisfy the accountants while the real "security" is the shared goal of finishing the work.

However even in high trust situations a written note is essential. People can die unexpectedly or get divorced or have a falling out. If the lender passes away their executor will need a written record of the debt to collect it for the estate. If the borrower dies their family needs to know that the money was a loan and not a gift. An unsecured note provides the "legal memory" that is necessary for any financial transaction to survive the unpredictable nature of human life.

Excellent Borrower Credit and Income

Lending to someone with a "gold plated" credit score and a high six figure income is one of the safest bets in finance. These individuals have spent years or decades proving that they are reliable and that they value their financial reputation above all else. For a private lender providing an unsecured note to such a person is a very low risk move. Even if the borrower has a temporary setback they likely have the resources and the pride to find a way to make things right.

In these cases asking for collateral could actually be counterproductive. High net worth individuals or successful business owners may be offended by the suggestion that their signature is not enough. An unsecured note is a way to show respect for their financial status and their history of success. It makes the transaction feel like a peer to peer deal rather than a predatory or overly cautious arrangement. It is about matching the "intensity" of the legal instrument to the "quality" of the borrower.

Lenders should still check that the borrower's income is stable and that they do not have any hidden liabilities. In the current Canadian market even wealthy people can be overleveraged with multiple mortgages and business debts. A quick review of a credit report and a confirmation of employment are still necessary steps for any unsecured loan. As long as the "numbers make sense" an unsecured note is a fast and efficient way to put capital to work with a high quality borrower.

Situations Where Collateral Is Unavailable

Sometimes a borrower has a great idea and a solid plan but no physical things to pledge. This is the classic "startup struggle." If a brilliant young developer is building a new app they may own nothing but a laptop and a pile of student debt. If you believe in the app and the developer then an unsecured note is the only way to provide the funding they need. You are investing in the "intellectual capital" of the person rather than the "physical capital" of a machine.

In these cases the unsecured note often serves as a "placeholder." It documents the debt today with the expectation that it will be paid back once the borrower finds more traditional success or receives a larger round of investment. It is a way to support innovation and entrepreneurship in Canada. Many of the country's most successful companies started with a few thousand dollars lent on an unsecured basis by a friend or a mentor who believed in the founder's potential.

Lenders who provide these loans are taking on a "venture risk" and they should be rewarded for it. This is why unsecured notes for startups often have higher interest rates or include clauses that allow the debt to convert into ownership in the future. While the note itself is unsecured it is part of a larger strategic bet on the borrower's future. It is a high risk and high reward strategy that has built many fortunes in the Canadian technology and service sectors.

Advantages and Disadvantages Comparison

Every financial decision is a balance of risks and rewards. For a lender a secured note offers a solid safety net but requires a lot of "homework" and ongoing maintenance. An unsecured note is fast and easy but it leaves you vulnerable to a total loss if the borrower's life falls apart. For a borrower the trade off is between the low cost of a secured loan and the high risk of losing an essential asset like their car or their business tools.

It is also important to consider the "social cost" of each note. A secured note is a very formal way to lend money and it can sometimes make a relationship feel cold or overly businesslike. An unsecured note is more of a "peer to peer" arrangement that can strengthen a bond of trust but it can also lead to a total breakdown in the relationship if the money is not paid back. There is no "perfect" note; there is only the note that is right for your specific situation and your specific level of comfort with risk.

The Canadian legal system provides tools to help both types of lenders but those tools have costs. A secured lender must pay for PPSA registrations and potentially for a bailiff. An unsecured lender must pay for a lawsuit and a Sheriff's writ. When you are deciding which note to use you must look at the "total cost of collection" and not just the face value of the loan. Sometimes the most expensive loan is the one that was the easiest to sign because it is the hardest one to collect.

Secured Note Advantages

The primary advantage of a secured note is the "hard protection" it provides. If the borrower defaults you have a physical thing you can take and sell to get your money back. This is a much more reliable recovery method than waiting for a court to garnish someone's wages. In the Canadian economy where jobs can be lost and businesses can close overnight having a claim on an asset like a car or a tractor is the ultimate form of financial security for a private lender.

For the borrower the main advantage is the lower cost of borrowing. Because the lender is safe they can afford to charge a much lower interest rate. This makes the loan more affordable and allows the borrower to keep more of their hard earned money. Secured notes also allow for larger loans and longer terms which gives the borrower the "breathing room" they need to make the money work for them. It is the most professional and sustainable way to access high levels of capital.

Another hidden advantage is the "priority" it gives the lender. If the borrower gets into a lot of debt the secured lender is the first one in line to get paid from the sale of the collateral. This "head of the line" status is a massive advantage in a bankruptcy or a liquidation. It ensures that the lender is not the one who "holds the bag" when the borrower's financial house comes crashing down. It is a defensive move that preserves the lender's wealth for their own needs.

Secured Note Disadvantages

The biggest disadvantage is the complexity of the "setup." You cannot just guess at the description of a car or a machine. You must be exact and you must perform a search and you must file your claim correctly with the provincial registry. If you make a mistake in the Identification Number or the debtor's name your security interest could be found invalid by a judge. This "technical risk" means that secured notes are not for people who want to rush through the paperwork.

For the borrower the disadvantage is the "stakes." If you miss a payment you could lose the very truck you need for work or the machine you need for your factory. This creates a high level of stress and leaves very little room for error. Secured loans also often come with "covenants" that require you to keep the asset insured and in good repair and allow the lender to inspect it. This can feel like the lender is looking over your shoulder which some people find very invasive.

There are also the "friction costs" of a secured note. You have to pay fees for the PPSA registration and potentially for an appraisal of the collateral. If the loan is for a small amount these fees can actually be a large percentage of the total debt. This makes secured notes less efficient for small personal favors and more suited for commercial or high value personal transactions where the cost of the paperwork is a small price to pay for the safety it provides.

Unsecured Note Advantages

The greatest advantage of an unsecured note is its "speed of execution." You can download a Promissory Note template and have it signed and the money transferred in the same hour. There is no need for appraisals or VIN checks or government filings. For an emergency loan to a friend or a quick business opportunity this speed is a major competitive advantage. It allows capital to move quickly to where it is needed most without being slowed down by bureaucracy.

For the borrower the advantage is "asset freedom." You do not have to worry about a lender seizing your car if you have a bad month. Your things stay your things. This flexibility is especially important for people who might need to sell their assets to move or to upgrade their business. An unsecured loan is a debt against the person not the property which gives the borrower much more control over their daily life and their long term financial decisions.

Unsecured notes are also the most "socially comfortable" way to lend. It does not feel like a cold business transaction. It feels like one person helping another. In many families and close professional groups this "soft" approach is necessary to maintain harmony and mutual respect. It acknowledges the debt without making the borrower feel like their property is being held hostage. It is a tool for building community and supporting those you trust.

Unsecured Note Disadvantages

The disadvantage is the "enforcement wall." If the borrower stops paying you have very few options that work quickly. You cannot just take their car. You have to go through the long and boring and expensive process of a lawsuit. If the borrower has moved to another province or has no assets you may never see a penny of your money again. The risk of a "total loss" is a constant shadow over every unsecured lending arrangement in Canada.

For the borrower the cost is the main downside. Because you are not offering security the lender will charge a much higher interest rate to cover their risk. This can make the loan a heavy burden over time. You may also find it much harder to borrow large amounts of money. If you need fifty thousand dollars for a house down payment you will likely find that very few people are willing to give it to you on an unsecured basis. It is a limited form of credit for small needs.

Finally there is the risk of "priority loss." If you get into financial trouble and have both secured and unsecured debts the secured lenders will take all your best assets. The unsecured lenders will then be forced to fight over whatever is left which often leads to aggressive collection tactics and wage garnishments. Being an unsecured borrower can actually be more stressful during a crisis because you have many different creditors all trying to reach into your paycheck at the same time.

How to Create Promissory Notes Using Ziji Legal Forms

1. Choose template

2. Add Parties' Details

Input the full legal names and current mailing addresses for both the person borrowing the money and the person providing the funds.

3. Add Term Details

Detail the exact principal amount being loaned along with the annual interest rate and the specific dates when each payment is due.

4. Add Final Details

Clearly describe any assets used as collateral and outline the specific penalties or legal actions that will follow if a default occurs.

5. Preview and print.

Carefully review the completed document for accuracy before printing the final copy for signing or saving it as a secure PDF.

Template-Specific Guidance

When you are ready to Create Promissory Note it is important to pick the template that matches the "intensity" of your deal. For a secured transaction you should use a template that includes a "Security Agreement" section. This section is where you will list the Identification Numbers for a vehicle or the serial numbers for a piece of equipment. It also includes the magic legal words that "grant" the lender a security interest in the property. This is the part that makes the note powerful in the Canadian legal system.

If you are making an informal loan a "Simple Promissory Note" template is the best choice. It is designed to be easy to read and understand for people who are not lawyers. It covers the basics like the amount and the interest rate and the due date without a lot of confusing legal jargon. This is perfect for family loans or small debts between friends where the goal is just to have a clear record of the agreement in case anyone's memory fails them later.

For business bridge loans you might consider a "Demand Note" template. This version does not have a set end date. Instead the lender can ask for the full payment at any time as long as they give the borrower a certain amount of notice like thirty or sixty days. This provides the lender with an "exit ramp" if they see the borrower's business starting to struggle. It is a very flexible tool for short term commercial financing and is a staple of the Canadian entrepreneurial scene.

Conclusion: Choose Your Note Type Based on Your Circumstances

Selecting between a secured and an unsecured promissory note is a vital decision that depends on your specific financial goals and your level of comfort with risk. A secured note provides the maximum possible protection for the lender through the use of collateral and is the gold standard for high value Canadian business transactions. An unsecured note offers a faster and simpler path for smaller loans where trust is the primary driver of the deal. Both instruments are governed by the federal Bills of Exchange Act and must comply with the strict new interest rate limits set by the Criminal Code of Canada. Using a professional Promissory Note template ensures that your agreement is legally robust and clearly understood by both parties. Regardless of the choice you make a written note is the best way to prevent disputes and preserve your professional and personal relationships. By taking the time to pick the right instrument today you are building a solid foundation for a successful financial future.

Professional comparison of secured and unsecured promissory notes in Canada under federal laws and interest rate limits.

Promissory Note FAQs

What else can a promissory note be called?

A promissory note can also be referred to as follows: demand note, IOU “I owe you”, loan agreement, or promise to pay agreement.

What is a promissory note?

A promissory note is a legal document where the borrower promises to repay the loan to the lender under the terms and conditions listed in the note.

What points should the promissory note cover?

You can create a promissory note using our simple template. A promissory note should have the terms as follows:

- Governing law: Select the province where the lender resides and the promissory note will be customized for that jurisdiction.

- Parties’ Info: Lender and borrower information such as full name and addresses.

- Loan amount: How much is the loan.

- Collateral: What security will be seized by the lender if the borrower fails to repay the loan. Describe the item in detail to ensure the collateral is not ambiguous. (e.g. list the VIN number if it is a vehicle, or a serial number if it is electronics)

- Interest payment: How much interest is being charged to the loan, if applicable

- Repayment schedule: How will the loan be paid back, whether in equal payments, a lump sum, or on demand. Payment schedules are flexible and can be made weekly, monthly, quarterly, semi-quarterly, and annually.

- Prepayment penalty: List the penalty for repaying the loan early, if applicable.

- Late penalty: How much additional interest will be charged if the payment is late, if applicable.

Do you need to notarize a promissory note?

Only the signature of the borrower and the lender are required to have a valid and enforceable promissory note. But if the loan is a substantial amount, it may be prudent to have it notarized since it adds a layer of authenticity if there are any future disputes regarding the loan.

What jurisdictions can use our promissory note?

You can use our template to create a legal and valid promissory note for the following jurisdictions:

|

Alberta

British Columbia

Manitoba

New Brunswick

Newfoundland and Labrador

Northwest Territories

Nova Scotia

Nunavat

Prince Edward Island

Saskatchewan

Yukon |

AB

BC

MB

NB

NL

NT

NS

NU

PE

SK

YT |

Author

Mandar Sonavane

|

Legal Content Writer at Ziji Legal Forms Inc.

Symbiosis International University

Mandar is a legal content writer specializing in the development of clear, practical, and easy-to-understand legal resources. With a strong focus on legal research, content creation, and plain-language writing, he works closely with our legal professionals to ensure that legal documents and educational materials are accurate, accessible, and user-friendly. At Ziji Legal Forms Inc., Mandar is responsible for researching legal topics, drafting and reviewing content, and helping transform complex legal concepts into straightforward guidance that empowers individuals and businesses to confidently navigate their legal needs.

Reviewed By

Histon Shek

|

General Counsel and Co-Founder at Ziji Legal Forms Inc.

University of Alberta

Histon Shek was called to the Alberta Bar in 2006. He holds a BA in Sociology and Philosophy and an LLB from the University of Alberta. As co-founder of Ziji Legal Forms Inc., he focuses on making legal documents accessible and affordable, overseeing legal integrity and content development.