TL;DR: - Ensure all documents comply with the Bills of Exchange Act to maintain negotiability and legal status.Interest rates must be expressed as an annual percentage to avoid the statutory five percent cap.

- Effective January 2025, the criminal interest rate for most loans is reduced to 35 percent APR.

- Vague repayment terms or missing dates can lead to a debt becoming statute barred under provincial limitation periods.

- Collateral descriptions must be highly specific and often require registration under the Personal Property Security Act.

- Written notes are superior to verbal agreements, which are difficult to prove and often viewed as gifts in family settings.

- Signatures from both parties and neutral witnesses provide the best evidence of a valid and consensual contract.

- You can use Ziji Legal Forms to create a legally valid Canadian Promissory Note

Introduction: Why Promissory Note Accuracy Matters

The creation of a Promissory Note Canada requires a high degree of precision to ensure that a financial obligation remains enforceable under federal and provincial statutes. A promissory note is a specialized legal instrument governed primarily by the Bills of Exchange Act. It represents an unconditional promise in writing to pay a sum certain in money at a fixed or determinable future time. Because these documents are often used as negotiable instruments, any ambiguity in their terms can lead to significant legal complications.

In the Canadian legal landscape, the accuracy of a promissory note serves as the foundation for debt recovery and conflict resolution. When a lender and a borrower enter into a loan agreement, the written record provides the necessary evidence to overcome the complexities of provincial court systems. Without a clearly defined and accurate document, a simple loan can transform into a protracted legal battle that drains resources and damages professional relationships.

Accuracy is particularly vital because Canadian courts apply strict interpretive rules to financial contracts. If a document contains vague language, judges may apply the principle of contra proferentem, which resolves any uncertainty against the party who drafted the note. This means that a lender who uses a poorly written Promissory Note template may find that the court interprets the terms in a way that favors the borrower. Ensuring that every clause is precise and legally compliant is the only way to safeguard an investment.

The legal environment in Canada is also subject to federal regulations like the Interest Act and the Criminal Code. These laws impose specific requirements on how interest is calculated and disclosed. For example, the Criminal Code was recently amended to lower the maximum allowable interest rate, effective January 1, 2025. An accurate note must reflect these current standards to remain valid. A failure to stay updated with these legislative shifts can result in a note becoming illegal and unenforceable.

Furthermore, the rise of the Online Promissory Note has made it easier for individuals to create their own documents. While this convenience is beneficial, it also increases the risk of including generic or non-compliant language. Accuracy in these digital documents ensures that they meet the same high standards as traditional paper notes. A well-crafted document provides peace of mind for both parties, knowing that their rights and obligations are clearly defined and protected by law.

This report explores the most common Mistakes in Promissory Notes within the Canadian context. By understanding these pitfalls, lenders and borrowers can better navigate the complexities of financial documentation. The goal is to produce a document that is robust enough to withstand judicial scrutiny while remaining clear enough for all parties to understand their commitments. Accuracy is not merely a technical requirement; it is a critical component of financial stability.

Mistake 1: Leaving Repayment Terms Vague or Missing

Why Clear Due Dates Matter

Repayment terms define the lifecycle of a Promissory Note Canada and determine when a lender has the right to demand their funds. Under the Bills of Exchange Act, a note must be payable on demand or at a fixed or determinable future time. If a note does not specify a date, it is legally treated as a demand note. While demand notes offer flexibility, they can create significant uncertainty for borrowers who may not be prepared to settle the full balance on short notice.

Clear due dates provide a structured framework for financial planning for both the lender and the borrower. When a date is fixed, the borrower knows exactly when they must have the liquidity available to satisfy the debt. This prevents accidental defaults and allows the borrower to manage their other financial obligations without fear of a sudden demand for payment. For the lender, a clear date provides a predictable cash flow and a specific point at which they can assess the success of the investment.

Without a specific due date, the calculation of interest also becomes complicated. If interest is meant to be paid periodically, the lack of a clear schedule makes it difficult to determine when a payment is officially late. This vagueness often leads to friction between parties, as they may have different interpretations of what constitutes a reasonable time for payment. Specificity in dates is the primary tool for avoiding these unnecessary disputes.

The importance of clarity extends to the end of the loan term. A maturity date signals the final settlement of the debt and the release of any security interests held by the lender. If this date is missing, the loan can theoretically exist indefinitely, which complicates the financial reporting and estate planning of both parties. A well-defined timeline ensures that the debt has a clear beginning, middle, and end, which is essential for professional financial management.

Impact on Enforcement

The ability to enforce a promissory note in a Canadian court depends heavily on the clarity of the repayment terms. When a borrower fails to pay, the lender must prove that the debt is currently due and owing. If the repayment terms are vague, a borrower can argue that the obligation has not yet matured, creating a significant hurdle for the lender. This defense can delay legal proceedings and increase the costs associated with debt recovery.

Provincial limitation periods also rely on clear dates to determine when a lender can no longer sue for a debt. In most Canadian provinces, such as Ontario, British Columbia, and Alberta, a lender has a two year window to start a lawsuit after a default occurs. If the note has a fixed due date, the calculation of this period is straightforward. However, if the date is missing or vague, determining when the clock started can become a major point of contention in court.

For demand notes, the situation is even more complex. In some jurisdictions, the limitation period might begin the moment the demand for payment is made and refused. In others, historical common law suggested the period could start as soon as the note was signed. Vague terms make it nearly impossible to predict how a judge will interpret these timelines. This uncertainty can result in a lender losing their legal right to recover their money simply because they waited too long to act.

Enforcement is also hindered when the note does not specify the method of payment. If a borrower claims they tried to pay but could not find the lender or did not know where to send the funds, the court may view the borrower more leniently. Providing a clear address or electronic transfer instruction within the note removes this excuse and strengthens the lender's position during enforcement proceedings. Clarity in the document translates directly to efficiency in the courtroom.

Essential Repayment Information

To avoid these Mistakes in Promissory Notes, the document should explicitly state the total principal amount and the exact dates for all payments. If the loan is to be repaid in a single lump sum, the maturity date should be clearly listed as a specific day, month, and year. If the loan involves installments, the note must detail the amount of each payment, the frequency of payments, and the start date for the first installment.

It is also important to define the currency of the repayment to avoid any confusion, especially in an increasingly global economy. While most domestic notes default to Canadian dollars, stating this clearly prevents any disputes if exchange rates fluctuate. The note should also specify whether payments are applied first to accrued interest or directly to the principal balance. This distinction can significantly affect the total cost of the loan over time.

Another critical piece of information is the place of payment. Section 183 of the Bills of Exchange Act notes that if a particular place is specified in the body of the note, it must be presented there for payment. Including this detail ensures that both parties are on the same page regarding the logistics of the transfer. Whether the payment is made via an Online Promissory Note portal or a physical bank draft, the instructions must be unambiguous.

Finally, the note should address the issue of prepayment. Borrowers often appreciate the flexibility to pay off a loan early to reduce interest costs. However, a lender may have structured their own finances around a specific interest return. The note should clearly state whether prepayment is allowed, if there are any penalties for early payment, and how much notice the borrower must provide. Documenting these details at the outset creates a predictable and fair environment for both parties.

Mistake 2: Missing or Unclear Interest Rate Details

Why Interest Terms Must Be Specific

The disclosure of interest is one of the most strictly regulated areas of Canadian contract law. The federal Interest Act requires that any interest rate in a written contract be expressed as an annual rate. Many lenders make the error of stating interest as a monthly or weekly percentage without providing the yearly equivalent. This lack of specificity is not just a stylistic issue; it is a legal failure that can strip a lender of their expected profit.

Specificity is required to ensure that borrowers can make an informed decision about the cost of credit. When an interest rate is expressed over a short period, the true cost of borrowing is often obscured. For example, a rate of two percent per month might sound manageable, but it represents an annual rate of over twenty four percent. The Interest Act aims to prevent this type of confusion by mandating transparency in the annualized cost of a loan.

In a Promissory Note Canada, interest terms must also define how the rate is calculated. If a note is silent on whether the interest is fixed or variable, disputes are likely to arise if market conditions change. Similarly, the note must clarify whether the interest is simple or compound. Simple interest is calculated only on the principal, while compound interest includes interest on previous interest. Without specific language, a court will likely default to the calculation that is most favorable to the borrower.

The consequences of missing interest details are severe. Under Section 3 of the Interest Act, if interest is agreed upon but no rate is fixed, the legal rate is set at only five percent per annum. This is often much lower than what a lender intended, especially in a high inflation environment. Specificity in the interest clause is the only way for a lender to ensure they receive the return they bargained for when the loan was initiated.

Calculating Interest Disputes

Disputes over interest calculations are common in Canadian courts, often centering on Section 4 of the Interest Act. This section states that if a contract provides for interest at a rate for any period less than a year, but does not state the equivalent annual rate, no interest exceeding five percent per annum is chargeable. This means that even if a borrower signed a note agreeing to a higher monthly rate, they can later challenge it if the annual rate was not explicitly disclosed.

Case law, such as the Cardtronics v Dawson decision, reinforces this strict interpretation. In that case, an interest rate of 1.5 percent per month was reduced to 5 percent per year because the annual rate was not stated. This serves as a stark warning to anyone using a generic Promissory Note template that does not include specific Canadian disclosures. A simple formatting error can result in a massive financial loss for the lender, as the court will not rewrite the contract to match the lender's original intent.

Another area of dispute involves the timing of interest accrual. If the note does not specify whether interest begins on the date of signing or the date the funds are actually advanced, the borrower may argue for the later date. Additionally, the day count convention used for calculations can be a point of friction. Most Canadian financial instruments use a 365 day year, but if the note is silent, small discrepancies in daily interest can add up over a multi-year loan.

The use of variable rates also introduces risk. If a note is tied to a bank prime rate, the document must clearly define which bank's rate is being used and how often the rate is adjusted. If the formula is too complex or ambiguous, a borrower may challenge the calculation of their balance. Clarity in these mathematical terms is essential for maintaining the enforceability of the note and avoiding expensive litigation over balance discrepancies.

Required Interest Specifications

To ensure a promissory note is fully compliant with Canadian law, the interest rate must always be expressed as an annual percentage. This should be the primary rate listed in the document. If a lender prefers to use monthly installments, they must still include a statement such as interest at a rate of one percent per month, which is equivalent to twelve percent per annum. This double disclosure satisfies both the logical needs of the parties and the legal requirements of the Interest Act.

Lenders must also be aware of the criminal interest rate under Section 347 of the Criminal Code. As of January 1, 2025, the government has lowered the criminal rate from an effective annual rate of 60 percent to an annual percentage rate of 35 percent. This 35 percent cap includes not just the interest but also all fees, commissions, and penalties associated with the loan. Any note that exceeds this threshold is illegal, and the interest provisions will likely be struck down entirely by a court.

When drafting an Online Promissory Note, it is also wise to specify whether the interest is simple or compound. If compound interest is intended, the note must state the frequency of compounding, such as monthly or semi-annually. This prevents the borrower from claiming that they only agreed to simple interest calculations. The note should also state that interest continues to accrue at the same rate after a default occurs, ensuring the lender is compensated for the delay in repayment.

Finally, the note should include a severability clause. This is a standard legal provision that states if any part of the note, such as the interest rate, is found to be illegal or unenforceable, the rest of the document remains in effect. This protects the lender from losing their entire principal just because they made a mistake in calculating the interest rate. By following these required specifications, a lender can create a robust and legally sound interest clause.

Mistake 3: Not Defining Late Fees or Penalty Terms

How Missing Penalties Weaken Enforcement

One of the most frequent Mistakes in Promissory Notes is the failure to include clear consequences for late payments. Without defined penalties, a borrower has less incentive to prioritize the repayment of the loan over other expenses. This lack of financial pressure can lead to chronic delinquency, forcing the lender to spend significant time and effort chasing down small payments. A note without penalties essentially provides the borrower with an interest free extension on their debt.

Missing penalties also make it more difficult for a lender to recover the administrative costs of dealing with a default. Every late payment requires communication, tracking, and sometimes the involvement of legal professionals. If these costs are not built into the note as late fees or collection charges, the lender must absorb them personally. This effectively reduces the actual interest rate the lender receives, as their profit is eaten away by the overhead of managing a delinquent borrower.

Furthermore, the absence of penalties can embolden a borrower during negotiations. If a borrower knows there is no immediate financial cost for being a week or a month late, they may treat the repayment schedule as a suggestion rather than a strict requirement. This can strain the personal or professional relationship between the parties, as the lender may feel disrespected or taken advantage of. Clear penalties act as a boundary that maintains the seriousness of the transaction.

In the eyes of a Canadian court, a lender who has not specified penalties may have a harder time proving the full extent of their damages. While a judge may award interest, they are unlikely to invent late fees that were never agreed upon in the original contract. By failing to define these terms at the outset, a lender forfeits a powerful tool for encouraging compliance and protecting their investment against the costs of delinquency.

Default Interest and Acceleration Clauses

To strengthen an Online Promissory Note, a lender should include a default interest rate and a robust acceleration clause. A default interest rate is a higher rate that takes effect only after a payment is missed. This higher rate compensates the lender for the increased risk of lending to someone who has shown a failure to meet their obligations. However, the default rate must be reasonable and must not push the total cost of borrowing above the 35 percent criminal interest cap.

An acceleration clause is arguably the most important enforcement tool in a promissory note. This clause gives the lender the right to declare the entire outstanding principal and interest due immediately if the borrower misses a single payment. Without this clause, a lender can typically only sue for the amount of the specific installment that was missed. This would require multiple, expensive lawsuits to recover the full debt if the borrower remains delinquent over a long period.

The combination of default interest and acceleration creates a strong deterrent against late payments. It informs the borrower that a single missed payment could result in the loss of their installment plan and the immediate requirement to settle the entire debt. This shifts the power balance back toward the lender and ensures that the borrower takes the repayment schedule seriously. These clauses are standard in professional Promissory Note Canada templates and are generally respected by Canadian courts.

Lenders should also specify that the borrower is responsible for all costs of collection, including reasonable attorney fees. In Canada, the general rule is that each party pays their own legal costs unless the contract states otherwise. Including this provision ensures that if the lender has to sue to recover their money, the borrower must cover the expenses of the litigation. This further protects the lender's principal and ensures that the default does not become a net loss for the lender.

Reasonable Penalty Requirements

While penalties are necessary, they must be drafted carefully to remain legal and enforceable under Canadian law. Canadian courts distinguish between a legitimate late fee and a penalty that is considered unconscionable. If a fee is so high that it bears no relationship to the lender's actual damages, a court may strike it down as an illegal penalty clause. The goal of a late fee should be to compensate the lender, not to excessively punish the borrower.

For example, a late fee that charges $100 for being one day late on a $500 payment might be viewed as a penalty rather than a reasonable fee. Such high charges can also inadvertently violate the Criminal Code if they push the annualized cost of the loan beyond 35 percent. Lenders must perform the math to ensure that their fees do not cross this line. A late fee that is found to be illegal can jeopardize the enforceability of the entire interest section of the note.

Reasonable penalties often include a small fixed fee for dishonoured cheques, typically around $20 to $50, which reflects the actual fees charged by banks. Another common approach is to allow a short grace period, such as five or ten days, before any late fees are applied. This demonstrates that the lender is acting in good faith and makes the penalty more likely to be upheld if the case goes to court. Fairness in drafting is a key element of legal enforceability.

Finally, the note should specify that the lender's decision not to charge a late fee on one occasion does not waive their right to do so in the future. This protects the lender if they choose to be lenient once but need to be strict later. By defining these terms clearly and reasonably, a lender can create a powerful set of incentives for the borrower while staying safely within the bounds of Canadian law.

Mistake 4: Forgetting Collateral Details or Description

When Collateral Should Be Included

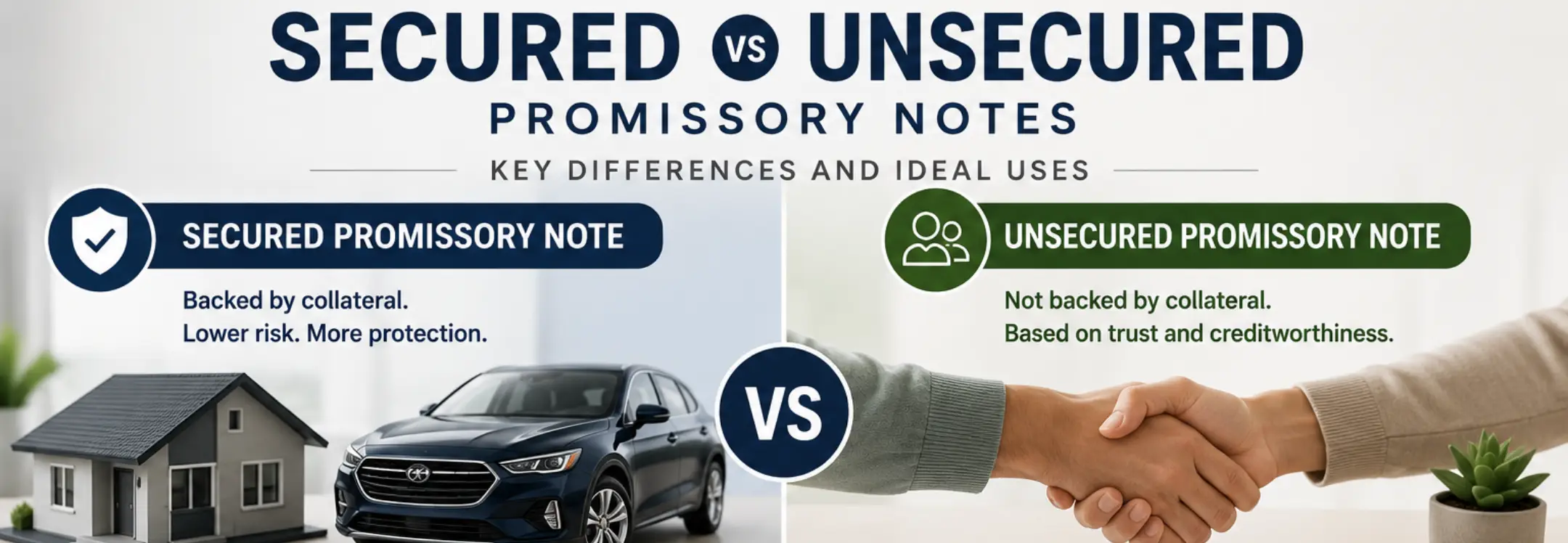

Collateral provides an essential layer of security for a lender, transforming a simple promise into a secured debt. In a Promissory Note Canada, collateral is property that the borrower pledges to the lender to guarantee the loan. If the borrower fails to pay, the lender has the legal right to seize and sell the collateral to recover the outstanding balance. Collateral should be included in any loan where the amount is significant or where the lender is unsure of the borrower's long-term ability to pay.

The inclusion of collateral is a standard risk management practice in professional lending. It changes the nature of the lender's position from being one of many creditors to being a secured party with a priority claim to a specific asset. This is particularly important for small business loans or loans for major purchases like vehicles or equipment. Without collateral, the lender is an unsecured creditor, which means they may receive nothing if the borrower enters bankruptcy.

Deciding when to include collateral often depends on the interest rate being charged. Secured loans typically have lower interest rates because the risk to the lender is reduced. If a lender is willing to provide a lower rate, they should insist on collateral to balance the risk. Conversely, if a borrower is unwilling to provide security, the lender should consider whether the interest rate accurately reflects the increased danger of an unsecured loan.

Finally, collateral can act as a psychological motivator for the borrower. Knowing that their car, equipment, or other valuable assets are on the line encourages the borrower to prioritize the loan. It creates a tangible consequence for default that goes beyond a simple mark on a credit report. In the Canadian context, using collateral is a proven way to reduce the likelihood of default and ensure a higher rate of recovery if things go wrong.

Risks of Unclear Collateral

The most significant risk associated with collateral is a vague or incomplete description in the note. A generic description like all of the borrower's equipment or my car is often insufficient for a court or a bailiff to identify the specific asset. If the borrower owns multiple cars or different types of equipment, an unclear description can render the security interest unenforceable. Clarity is the only way to ensure the lender's rights are protected.

In Canada, the Personal Property Security Act or PPSA governs most security interests in movable property. To be effective against third parties, such as other creditors or a bankruptcy trustee, the security interest must be perfected, usually through registration in a provincial PPSA registry. If the description in the promissory note does not match the information in the PPSA registration, the lender may lose their priority. This means another creditor with a better description could take the asset first.

Another risk is failing to address the location of the collateral. If a borrower moves the asset to another province, the lender's registration in the original province may become ineffective after a certain period. An Online Promissory Note should include a clause that requires the borrower to keep the collateral in a specific location and notify the lender of any move. This allows the lender to update their PPSA registrations and maintain their security interest across jurisdictional lines.

Unclear collateral terms also complicate the process of repossession. If the note does not specify the lender's right to enter the borrower's property or the procedures for selling the asset, the lender may face legal challenges during the enforcement phase. In some cases, a borrower might sue a lender for wrongful seizure if the collateral description was too broad or inaccurate. Precise wording in the note is the best defense against these costly and time-consuming counter-claims.

Complete Collateral Information

A well-drafted Promissory Note template must include a detailed and unique description of the pledged asset. For vehicles, this includes the year, make, model, and the unique seventeen digit Vehicle Identification Number or VIN. For industrial equipment or electronics, the manufacturer, model number, and serial number are essential. For general assets like inventory, the description should follow the categories defined in the provincial PPSA to ensure compatibility with registry systems.

The collateral section should also include representations by the borrower that they actually own the asset and that it is free from other liens. This protects the lender from discovering later that the borrower pledged an asset they did not truly control. The note should also require the borrower to maintain insurance on the collateral and name the lender as a loss payee. This ensures that if the asset is destroyed, the insurance proceeds will go directly to paying down the loan.

Lenders should also specify the conditions under which they can inspect the collateral. Regular inspections ensure that the asset is being properly maintained and has not been sold or damaged. The note should also prohibit the borrower from selling, leasing, or further encumbering the asset without the lender's express written consent. These restrictions are vital for maintaining the value of the security throughout the life of the loan.

Finally, the note must outline the specific rights of the lender upon default. This includes the right to take possession of the collateral, the right to repair or prepare it for sale, and the right to sell it via public or private auction. It should also state that if the sale of the collateral does not cover the full balance of the loan, the borrower remains liable for the remaining deficiency. This comprehensive approach ensures that the collateral provides the maximum possible protection for the lender's capital.

Mistake 5: Not Specifying What Constitutes Default

Ambiguity About Default Conditions

Default is the trigger for all enforcement actions, yet many people fail to define it broadly enough in their Promissory Note Canada. Most borrowers and lenders assume that default only occurs when a payment is missed. While this is the primary cause, there are many other events that can jeopardize a lender's ability to be repaid. If these events are not listed in the note, the lender may be legally forced to stand by while the borrower's financial situation collapses.

Ambiguity regarding default conditions can leave a lender paralyzed during a crisis. For example, if a borrower becomes insolvent or files for bankruptcy, the lender needs to be able to act immediately to claim their place in line for the borrower's assets. If the note only allows for enforcement upon a missed payment, the lender might have to wait weeks or months before they can take action. By that time, the borrower's remaining assets may have been seized by other, more proactive creditors.

Other non-payment defaults include the death of the borrower, the dissolution of a corporate borrower, or the seizure of the borrower's assets by the government. These are all critical signs that the loan is at risk. If these are not specified as defaults, the lender has no clear path to accelerate the debt or protect their collateral. A comprehensive definition of default ensures that the lender can react to a wide variety of threats to their investment.

Furthermore, a breach of any other term in the note should also be considered a default. This includes failing to keep collateral insured, providing false information in the loan application, or moving the collateral out of the jurisdiction without permission. If the note is silent on these issues, the borrower can violate the spirit of the agreement with no immediate legal consequence. Clarity in default conditions is the only way to ensure the borrower follows all the rules, not just the repayment schedule.

Enforcement Challenges

The primary challenge of a vague default clause is that it makes enforcement in court much more difficult. In Canada, judges will look to the written contract to see if the lender had the legal right to take the actions they did. If a lender seizes a vehicle or demands full payment without a clear contractual trigger, the borrower can sue for breach of contract or even conversion. Precise default language is the lender's shield against these legal counter-attacks.

Another challenge involves the requirement of notice. Canadian law often expects a lender to behave reasonably and provide a borrower with a fair chance to fix a problem. If the note does not specify how notice must be given or how long a borrower has to cure a default, the parties will inevitably end up in a dispute over whether the lender was too aggressive. This can lead to a judge staying the enforcement proceedings, costing the lender time and money.

Vague default conditions also complicate the application of the limitations period. As noted previously, a lender generally has two years from the discovery of a claim to sue. If the default condition is not clearly defined, it is difficult to pin down the exact date when the claim was discovered. A borrower may argue that the default actually happened much earlier than the lender claims, potentially making the lawsuit invalid because the two year window has passed.

For lenders using an Online Promissory Note, the lack of a clear default section can also make it harder to sell the note to a collection agency or another investor. Professional buyers of debt look for documents with clear, unambiguous triggers for enforcement. If the note is poorly drafted, it will be seen as a higher risk and will have a much lower resale value. Specificity in default terms is essential for maintaining the liquidity and value of the promissory note.

Essential Default Language

A professional Promissory Note template should include a detailed list of events that constitute a default. At a minimum, this must include failure to make a principal or interest payment within the allowed grace period. It should also include any representation or warranty made by the borrower being found to be false or misleading. Bankruptcy, insolvency, and the appointment of a receiver over the borrower's assets are also standard default triggers that must be included.

Lenders should also consider including a cross-default clause. This provision states that if the borrower defaults on any other debt they have with the same lender, it automatically triggers a default on the current promissory note. This allows the lender to protect themselves across multiple transactions if the borrower begins to show signs of systemic financial trouble. It is a powerful tool for consolidated risk management in professional and commercial lending.

The note must also clearly define the cure period. For a missed payment, a cure period of five to ten business days after written notice is common. For non-monetary defaults, such as failing to provide proof of insurance, a longer period like thirty days might be appropriate. Clearly stating these timelines prevents arguments about fairness and ensures that both parties know exactly when the situation moves from a simple mistake to a full legal default.

Finally, the document should specify the remedies available to the lender upon default. This includes the right to accelerate the debt, the right to increase the interest rate to the default rate, and the right to take possession of any collateral. The note should explicitly state that these remedies are cumulative, meaning the lender can use any or all of them as they see fit. This provides the lender with the maximum possible flexibility to resolve the default and recover their funds.

Mistake 6: Relying on Verbal Agreements Instead of Written Documentation

Problems Without Written Records

In the world of informal lending, many people rely on verbal agreements, especially when dealing with friends or family members. However, this is one of the most dangerous Mistakes in Promissory Notes. The most immediate problem with a verbal agreement is the fallibility of human memory. Over months or years, the lender and borrower may develop completely different recollections of the interest rate, the repayment schedule, or even the total amount borrowed.

When these memories inevitably clash, the lack of a written record turns a simple misunderstanding into a major conflict. Without a document to refer to, there is no objective way to settle the dispute. This often leads to the permanent breakdown of personal relationships, as both parties feel that the other is being dishonest. A Promissory Note Canada provides a single source of truth that protects the social fabric of the lending relationship by removing ambiguity.

Verbal agreements also offer no protection against the death or disability of either party. If a borrower passes away, their estate executor is legally obligated to protect the assets of the deceased. Without a signed promissory note, an executor may refuse to pay the debt, arguing that there is no evidence the money was a loan rather than a gift. Similarly, if the lender dies, their heirs may never even know that the money was owed to them, resulting in a total loss of the family's assets.

Furthermore, a verbal agreement provides no mechanism for interest calculation or penalty enforcement. In Canada, if you want to charge interest above five percent, you must have it in a written contract. If your agreement is only verbal, you are legally limited in what you can collect, regardless of what the borrower originally promised. Relying on a handshake is a guaranteed way to lose a significant portion of your potential return on a loan.

Legal Enforceability Requirements

Proving a verbal contract in a Canadian court is an uphill battle. The person seeking to enforce the loan must provide evidence of an offer, an acceptance, and consideration. While bank statements might show a transfer of funds, they do not prove the terms of the deal. The borrower could easily claim the money was a gift, a repayment for a previous debt, or an investment in a joint venture. Overcoming these defenses without a written note is expensive and often impossible.

In some provinces, the Statute of Frauds requires certain contracts to be in writing to be enforceable. This includes agreements that cannot be fully performed within one year and contracts where one person agrees to be a guarantor for another's debt. If your verbal loan falls into these categories, it is legally void from the start. A written Online Promissory Note is the only way to ensure your agreement complies with these age-old legal requirements for enforceability.

The limitation period also becomes a major problem with verbal agreements. Since there is no written proof of when a payment was due, it is difficult for a court to determine when the two year period for a lawsuit began. A borrower can argue that the debt became due much earlier than the lender claims, potentially making the lender's lawsuit too late to proceed. The lack of a written date creates a legal ambiguity that borrowers can easily exploit to avoid repayment.

Furthermore, Canadian law often applies the presumption of advancement in family situations. This means that if a parent gives a large sum of money to a child, the court will presume it was a gift unless there is clear written evidence to the contrary. Without a promissory note, a parent may find that they cannot legally recover a loan from their own child if the relationship sours. A written document is the only way to overcome this presumption and ensure the law treats the transaction as a binding loan.

Benefits of Written Documentation

The most obvious benefit of a written promissory note is clarity. It ensures that both parties are on the same page regarding every aspect of the loan, from the interest rate to the collateral. This clarity reduces the likelihood of future disputes and provides a professional framework for the entire transaction. Even if the loan is between close friends, a written document shows that both parties take the obligation seriously and value their relationship enough to protect it.

A written note also creates a negotiable instrument under the Bills of Exchange Act. This means the lender can sell the note to a third party or a collection agency if they need immediate cash. This provides the lender with liquidity and options that are simply not available with a verbal agreement. You cannot sell a verbal promise to a bank or a debt buyer. Having a professional document turns a personal debt into a valuable financial asset.

In terms of enforcement, a written note provides the lender with a strong cause of action. In many cases, a lender can skip a full trial and apply for a summary judgment based on the signed note. This is a much faster and cheaper way to get a court order for repayment. If the borrower's signature is on the document and the terms are clear, the borrower has very few defenses they can raise. This efficiency is the primary reason why professional lenders never rely on verbal deals.

Finally, a written note allows for the inclusion of specialized clauses that protect the lender, such as the right to collect legal fees or the right to accelerate the debt upon default. These protections are simply not available in a verbal agreement. By using a Promissory Note template, a lender can ensure they have every possible legal tool at their disposal to ensure their money is returned. Putting it in writing is the single most important step any lender can take.

Mistake 7: Not Getting Both Party Signatures or Leaving Notes Undated

Why Signatures Are Essential

A signature is the ultimate proof of consent and the cornerstone of any binding contract. In the context of a Promissory Note Canada, the signature of the borrower is a mandatory requirement under the Bills of Exchange Act. This signature confirms that the borrower has read the terms, understands their obligations, and has entered into the agreement of their own free will. Without this mark, the document is nothing more than a draft and has no power in a court of law.

Signatures also provide a critical link between the legal document and the actual person who owes the money. In a digital world, where identity theft is a constant threat, having a clear and verified signature is more important than ever. If a borrower later claims they never agreed to the loan, their signature serves as the primary piece of evidence to prove otherwise. It is the physical manifestation of their commitment to repay the debt.

For corporate borrowers, the signature is even more complex. The note must be signed by an authorized representative of the company, such as a director or an officer. The signature block should clearly state the person's title and the full legal name of the corporation. If this is done incorrectly, the lender may find that the individual is not personally liable, or that the corporation can disavow the debt because the person who signed did not have the authority to do so.

While the law technically only requires the borrower to sign for the note to be a valid bill of exchange, it is highly recommended that the lender signs as well. This creates a reciprocal agreement and prevents any argument that the document was a unilateral offer that was never accepted. When both parties sign, it shows a mutual intent to be bound by the terms, which is the gold standard for any legal agreement in Canada.

Problems Caused by Unsigned Notes

The most obvious problem with an unsigned note is that it is entirely unenforceable. If a lender tries to sue a borrower based on an unsigned document, the case will be dismissed almost immediately. The court will not take away a person's property or garnish their wages based on a piece of paper that they never formally accepted. An unsigned note is essentially a zero dollar asset for the lender.

Partially signed notes also create massive legal headaches. If there are multiple borrowers but only one has signed, the lender can only pursue that one person for the debt. The other borrowers can walk away with no liability, leaving the lender with only half the security they expected. This is a common error in joint ventures or family loans where one spouse signs but the other does not. Every person who is meant to be liable must sign the document individually.

Leaving a note undated is another serious mistake that can lead to a variety of disputes. The date of the note is used to calculate the starting point for interest and is often the reference for the repayment schedule. If a note says it is due one year from the date of this agreement but there is no date, the maturity date becomes a moving target. This ambiguity can be used by a borrower to stall payments for months while they argue over when the clock actually started.

An undated note also makes it difficult to apply the limitation period for lawsuits. Since the court cannot determine when the contract began, it is harder to determine when it was breached and when the two year window for filing a claim expired. This can lead to the lender's lawsuit being thrown out of court simply because they cannot prove they filed it in time. A date is a small detail that has massive implications for the legal lifespan of a promissory note.

Proper Signature Procedures

To ensure a Promissory Note Canada is as strong as possible, both parties should sign the document in the presence of an independent witness. A witness is a neutral third party who can testify later that they saw the parties sign the document and that everyone appeared to be of sound mind and acting without coercion. While not a strict requirement for all notes, having a witness adds an extra layer of protection that is highly valued in the Canadian legal system.

The signature blocks should be clear and include the printed name of the signer, their title if applicable, and the date of signing. For larger loans or those involving collateral, it is often wise to have the signatures notarized by a Notary Public. A notary verifies the identity of the signers by checking their government-issued ID, making it virtually impossible for a borrower to later claim they were a victim of forgery. This is a standard procedure for any professional or high-value transaction.

When using an Online Promissory Note, parties should ensure they are using a platform that provides secure digital signatures that comply with provincial electronic commerce laws. These digital signatures are legally equivalent to physical ones and often come with a digital audit trail that shows exactly when and where the document was signed. This provides an even higher level of security and convenience than traditional paper signatures, making it an excellent choice for modern lenders.

Finally, every party should receive a fully executed original copy of the note. For the lender, the original document is their most important piece of evidence. If the case goes to court, the judge will typically require the original note to be produced under the best evidence rule. Storing the signed and dated note in a secure, fireproof location or a safe deposit box is the final step in protecting a significant financial investment. Proper procedures at the time of execution prevent massive problems in the future.

Mistake 8: Using Outdated or Incomplete Templates

Problems with Generic Forms

The internet offers a vast array of legal forms, but many of them are entirely unsuitable for use in Canada. One of the most common Mistakes in Promissory Notes is using a generic template that was drafted for the United States or another jurisdiction. These forms often reference laws, such as specific US state codes or usury limits, that have no application in Canada. Using such a form can make your entire agreement appear unprofessional and potentially unenforceable in a Canadian court.

Generic forms also tend to be overly simplistic. They may cover the basic amount and the parties but miss the nuanced clauses that provide real protection for a lender. For example, a basic form might not include a clear acceleration clause or a provision for collecting legal fees. Without these specialized terms, a lender is left with a weak legal instrument that offers very little leverage if the borrower decides to stop paying.

Furthermore, generic templates are often not updated to reflect changes in federal law. A form from even a few years ago might not comply with the new 2025 Criminal Code amendments regarding interest rates. Using an outdated form could result in you inadvertently charging a criminal rate of interest, which not only voids your interest provisions but could also lead to criminal charges. Laws are dynamic, and your legal documents must be dynamic too.

Another issue with generic forms is that they do not address provincial differences. While the Bills of Exchange Act is federal, many other aspects of lending are governed by provincial law, such as the PPSA for collateral or the Limitations Act for lawsuits. A one-size-fits-all form will inevitably miss these critical local requirements, leaving the lender exposed to risks they didn't even know existed. Only a Canada-specific template can provide the necessary local compliance.

Missing Critical Clauses

An incomplete Promissory Note template is often missing the boilerplate clauses that act as a safety net for the parties. A prime example is the severability clause. This provision states that if a court finds one part of the note to be illegal or invalid, the rest of the document remains in effect. Without this clause, a single error in your interest rate calculation could cause a judge to throw out the entire note, meaning you could lose your right to even the principal.

Another common omission is the governing law clause. This clause specifies which province's laws will be used to interpret the note and which courts will have the power to hear any disputes. This is vital if the lender and borrower live in different provinces, such as Ontario and British Columbia. Without a governing law clause, the parties may waste thousands of dollars in a legal battle just to decide where the case should be heard.

Many basic templates also fail to include a non-waiver clause. This clause protects a lender who chooses to be lenient on one occasion. For example, if a borrower is late once and the lender chooses not to charge a late fee, the non-waiver clause ensures the lender can still charge late fees for any future delays. Without this protection, a borrower could argue that the lender's previous kindness has permanently changed the terms of the contract, a defense known as promissory estoppel.

Finally, an incomplete template often misses the entire section on collateral and security interests. A note that is meant to be secured but uses an unsecured template is a major failure of risk management. Professional Promissory Note Canada templates include specific sections for describing collateral and granting a security interest, ensuring that the lender has more than just a promise to rely on. Missing these sections is a mistake that can lead to a total loss of funds.

Selecting Current Templates

The only way to ensure your financial agreements are sound is to use a Promissory Note template that is specifically designed for the Canadian market and updated for the current year. This is particularly important given the major shift in interest rate laws that took effect on January 1, 2025. A current template will have the built-in safeguards to keep your APR below the 35 percent limit and ensure your disclosures meet the standards of the Interest Act.

When selecting a template provider, look for one that understands the federal and provincial landscape. The platform should offer specialized forms that address the requirements of the Bills of Exchange Act while providing the flexibility to add provincial-specific details like PPSA descriptions. A high-quality Online Promissory Note tool will guide you through these choices, ensuring that you don't miss any critical sections or include conflicting terms.

You should also choose a template that is easy to read and professionally formatted. A document that uses clear, modern language rather than dense legalese is more likely to be understood by both parties and respected by a court. It reduces the chance of a borrower claiming they were confused by the terms and provides a solid foundation for a healthy financial relationship. Professionalism in your documentation reflects professionalism in your lending practices.

Finally, the best templates are those that allow for full customization. Every loan has unique terms, from grace periods to installment schedules. A static PDF is rarely enough to capture these details. Using a platform like Ziji Legal Forms allows you to build a note that is tailored to your specific needs while maintaining a high standard of legal compliance. This combination of flexibility and structure is the best way to avoid the mistakes that plague so many private loans.

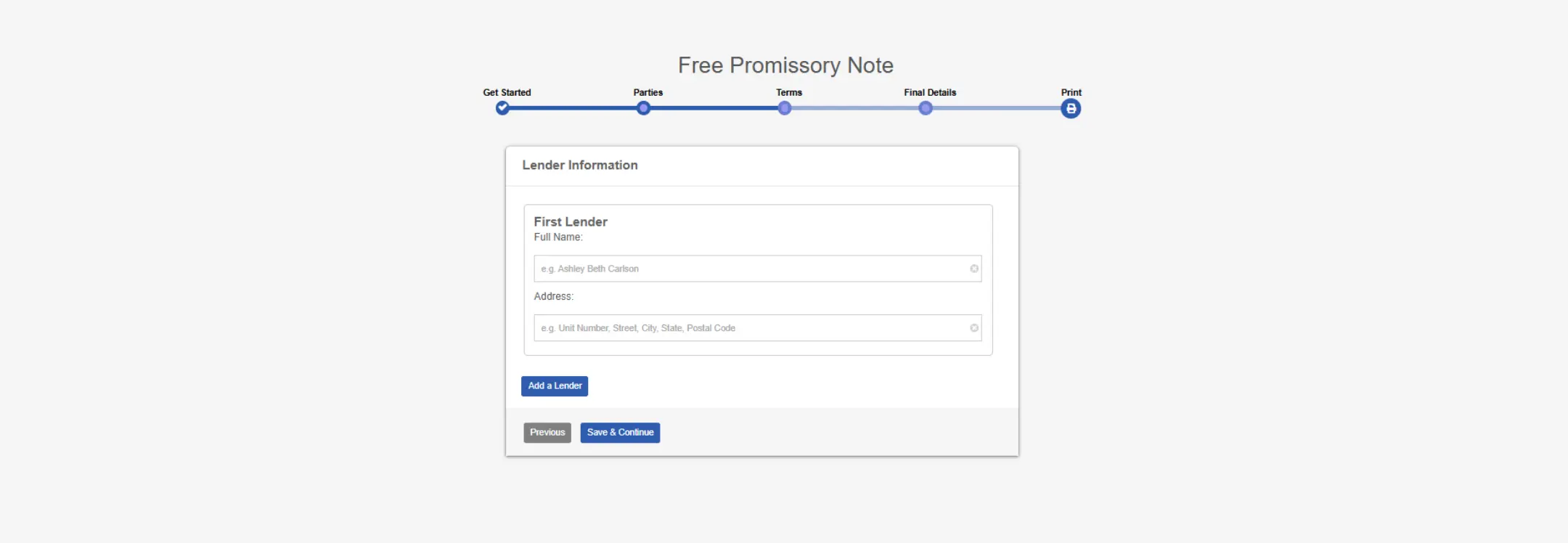

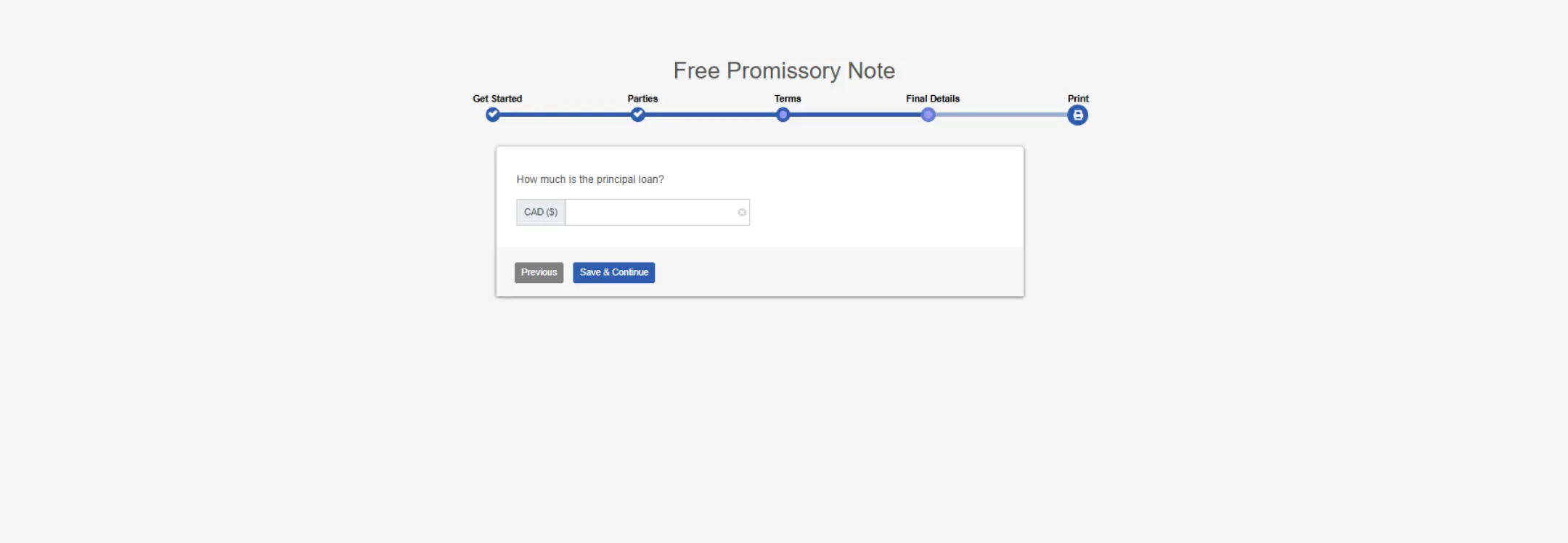

How to Create a Promissory Note Using Ziji Legal Forms

1. Choose template

2. Add Party Details

Enter the full legal names and physical mailing addresses for both the lender and the borrower to establish clear legal identification.

3. Add Term Details

Specify the principal amount, the annual interest rate, and the exact repayment schedule to create a binding financial agreement.

4. Add Preview and Print

Review the completed draft for accuracy and completeness before printing the final version to be signed and witnessed.

Using Ziji Templates Reduces Common Mistakes

The Ziji Legal Forms platform is specifically designed to eliminate the risks associated with manual drafting. By following a guided, logical workflow, the system ensures that users do not leave essential repayment terms vague or missing. The prompts for due dates and installment amounts prevent the creation of unintended demand obligations, ensuring that both parties have a clear and enforceable schedule for the return of funds.

Ziji also solves the complex problem of interest rate disclosure. The platform automatically formats interest terms to comply with Section 4 of the Interest Act, expressing rates as an annual percentage to avoid the statutory five percent cap. Furthermore, the built-in compliance checks for the 2025 Criminal Code amendments ensure that no note accidentally charges a criminal rate of interest, protecting lenders from the severe legal consequences of overcharging.

The risk of unclear collateral is also addressed through the specialized sections of the Promissory Note Canada template. Ziji provides the necessary space for detailed asset descriptions, such as VINs and serial numbers, which are required for effective PPSA registration. This ensures that a lender's security interest is robust and ready for perfection in any provincial registry. By providing these structured fields, Ziji helps users create secured notes that offer real protection rather than just a false sense of security.

Finally, using a professional platform ensures that all critical boilerplate clauses, from severability to governing law, are included by default. These clauses are the silent guardians of a legal agreement, providing protection in scenarios that most people never consider. Ziji transforms a complex and risky legal task into a simple, step-by-step process, allowing anyone to produce a professional, compliant, and highly enforceable promissory note in minutes.

Conclusion: Protect Your Loan with Complete and Accurate Promissory Notes

Accuracy in a promissory note is the primary defense against financial loss and legal frustration in Canada. By following the Bills of Exchange Act and respecting modern interest rate limits, you ensure your agreement remains enforceable in court. Using professional tools from Ziji Legal Forms allows you to avoid vague terms and missing signatures while staying fully compliant with Canadian law.

Promissory Note FAQs

What else can a promissory note be called?

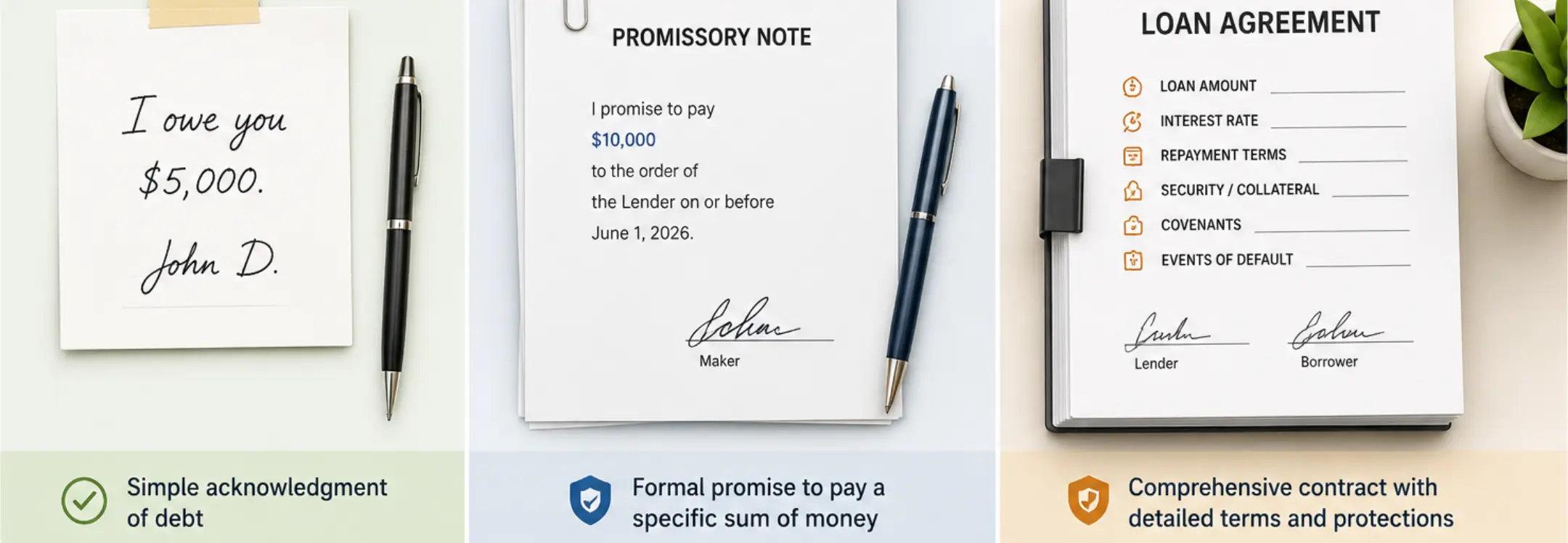

A promissory note can also be referred to as follows: demand note, IOU “I owe you”, loan agreement, or promise to pay agreement.

What is a promissory note?

A promissory note is a legal document where the borrower promises to repay the loan to the lender under the terms and conditions listed in the note.

What points should the promissory note cover?

You can create a promissory note using our simple template. A promissory note should have the terms as follows:

- Governing law: Select the province where the lender resides and the promissory note will be customized for that jurisdiction.

- Parties’ Info: Lender and borrower information such as full name and addresses.

- Loan amount: How much is the loan.

- Collateral: What security will be seized by the lender if the borrower fails to repay the loan. Describe the item in detail to ensure the collateral is not ambiguous. (e.g. list the VIN number if it is a vehicle, or a serial number if it is electronics)

- Interest payment: How much interest is being charged to the loan, if applicable

- Repayment schedule: How will the loan be paid back, whether in equal payments, a lump sum, or on demand. Payment schedules are flexible and can be made weekly, monthly, quarterly, semi-quarterly, and annually.

- Prepayment penalty: List the penalty for repaying the loan early, if applicable.

- Late penalty: How much additional interest will be charged if the payment is late, if applicable.

Do you need to notarize a promissory note?

Only the signature of the borrower and the lender are required to have a valid and enforceable promissory note. But if the loan is a substantial amount, it may be prudent to have it notarized since it adds a layer of authenticity if there are any future disputes regarding the loan.

What jurisdictions can use our promissory note?

You can use our template to create a legal and valid promissory note for the following jurisdictions:

|

Alberta

British Columbia

Manitoba

New Brunswick

Newfoundland and Labrador

Northwest Territories

Nova Scotia

Nunavat

Prince Edward Island

Saskatchewan

Yukon |

AB

BC

MB

NB

NL

NT

NS

NU

PE

SK

YT |

Author

Mandar Sonavane

|

Legal Content Writer at Ziji Legal Forms Inc.

Symbiosis International University

Mandar is a legal content writer specializing in the development of clear, practical, and easy-to-understand legal resources. With a strong focus on legal research, content creation, and plain-language writing, he works closely with our legal professionals to ensure that legal documents and educational materials are accurate, accessible, and user-friendly. At Ziji Legal Forms Inc., Mandar is responsible for researching legal topics, drafting and reviewing content, and helping transform complex legal concepts into straightforward guidance that empowers individuals and businesses to confidently navigate their legal needs.

Reviewed By

Histon Shek

|

General Counsel and Co-Founder at Ziji Legal Forms Inc.

University of Alberta

Histon Shek was called to the Alberta Bar in 2006. He holds a BA in Sociology and Philosophy and an LLB from the University of Alberta. As co-founder of Ziji Legal Forms Inc., he focuses on making legal documents accessible and affordable, overseeing legal integrity and content development.