Promissory Note vs Loan Agreement vs IOU - Which one should you use

TL;DR

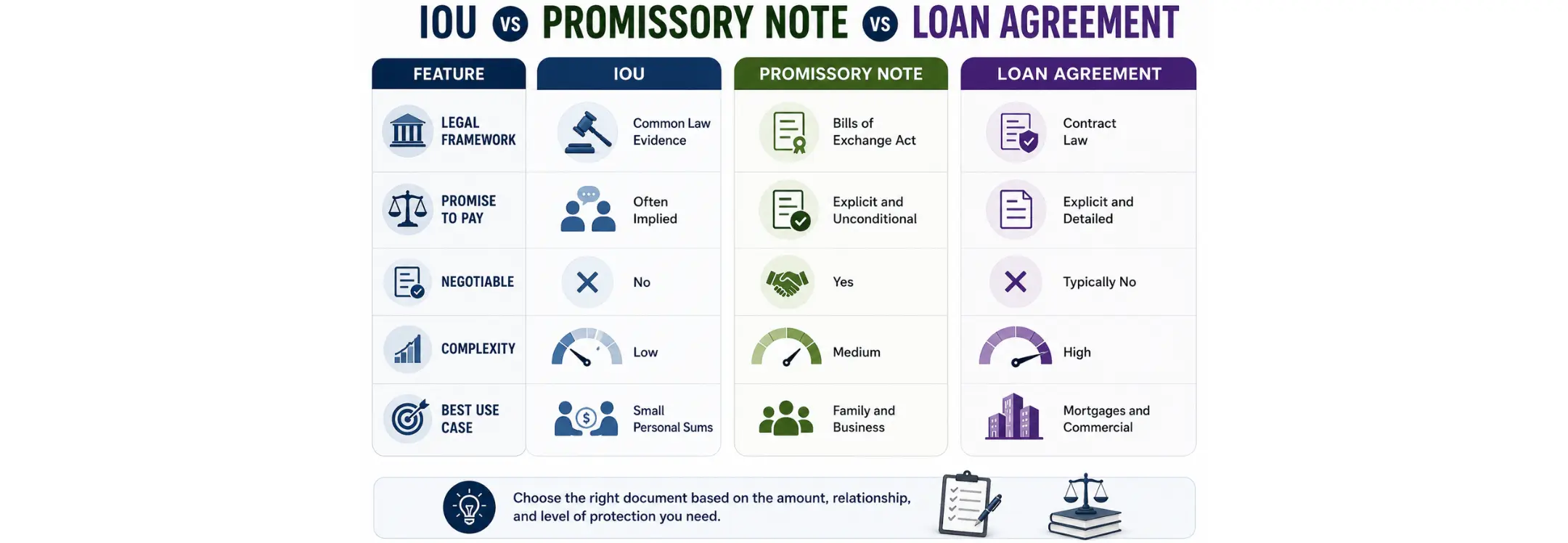

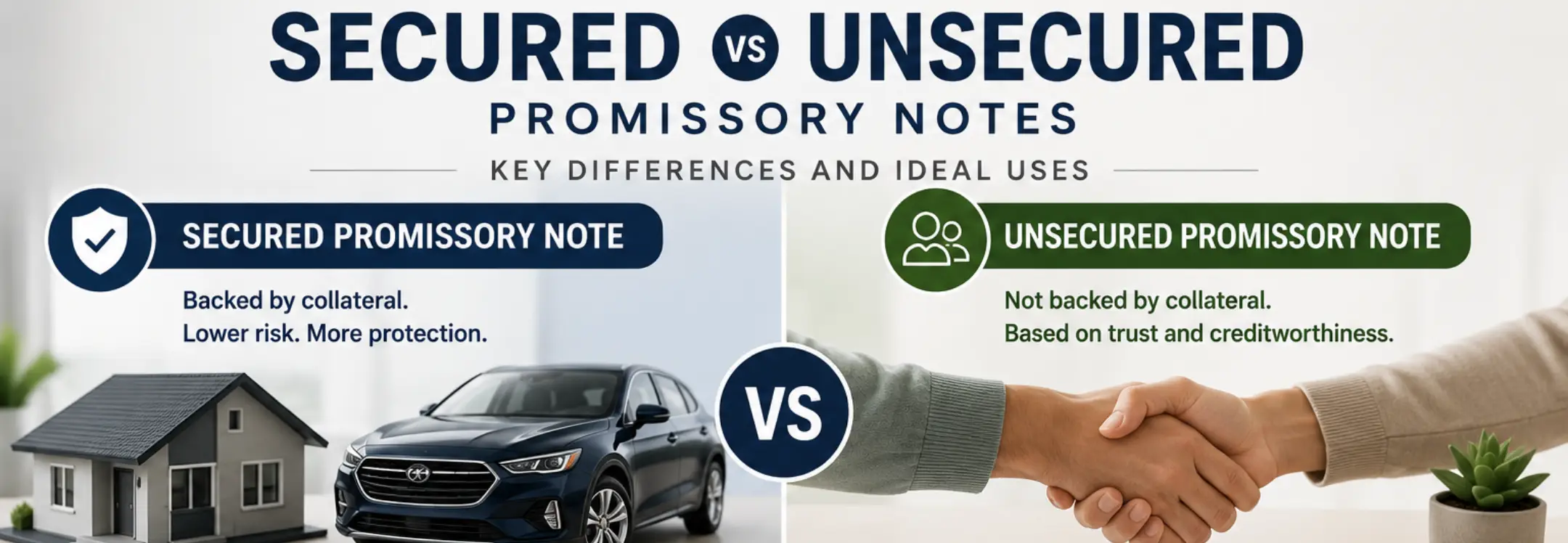

Promissory notes are formal negotiable instruments governed by federal law that provide an unconditional promise to pay a specific sum of money.

Loan agreements are comprehensive bilateral contracts that outline extensive terms, covenants, and security interests for large or complex transactions.

IOUs are informal acknowledgments of debt that serve as evidence of a liability but often lack specific repayment terms and a formal promise to pay.

As of the 2025, the criminal interest rate in the country of Canada is capped at an annual percentage rate of 35 percent for most personal and small business loans.

Enforcement of any debt instrument is subject to provincial limitation periods, which are typically two years from the date of default in the majority of Canadian provinces.

Ziji Legal Form's provides an easy-to-use online template to help you create Promissory Notes.

Why These Three Documents Get Confused?

The primary reason for confusion among these three documents is their shared objective of recording a debt. In casual conversation, individuals often use these terms interchangeably without realizing that each carries distinct legal consequences under the laws of the country of Canada. Many people believe that any piece of paper signed by a borrower is sufficient to guarantee repayment, but the specific wording used can significantly alter the rights of the lender and the obligations of the borrower.

The linguistic overlap in the lending industry contributes to this lack of clarity. A borrower might refer to their obligation as a note while the lender views the transaction as a formal loan agreement. Because all three documents serve as written evidence of a financial transfer, the average person may not appreciate the technical requirements of the federal Bills of Exchange Act compared to the general principles of contract law. This confusion is particularly prevalent in private lending scenarios where parties may not seek professional legal counsel.

Another factor is the historical evolution of these documents. In earlier periods of Canadian history, informal notes and receipts were the standard for local commerce. As the legal system became more sophisticated, the distinction between a simple acknowledgment of debt and a negotiable instrument became sharper. Today, the federal government regulates certain aspects of these documents, while provincial governments oversee others, leading to a complex web of rules that can baffle the uninitiated lender.

The perceived simplicity of an IOU often masks its legal limitations, leading lenders to believe they have more protection than they actually do. Conversely, the complexity of a full loan agreement can sometimes scare off potential borrowers in a family setting, causing parties to default to a promissory note without fully understanding its negotiable nature. Understanding the nuances of each instrument is the first step toward managing financial risk in any lending transaction.

What is a Promissory Note

A promissory note is defined under the federal Bills of Exchange Act as an unconditional promise in writing made by one person to another. The maker of the note must sign it and engage to pay a sum certain in money either on demand or at a fixed or determinable future time. This definition, found in Section 176 of the Act, is the cornerstone of how these instruments are treated by Canadian courts.

To qualify as a promissory note in the country of Canada, the document must be absolutely unconditional. If the promise to pay is dependent on a specific event, such as the borrower receiving an inheritance or selling a piece of property, the document is no longer a promissory note under the federal Act. It might still be a contract, but it loses the unique legal status and the ease of transferability that comes with being a negotiable instrument.

The concept of a sum certain is another essential requirement. The note must specify exactly how much money is owed. While the note can include interest, the rate and the method of calculation must be clear so that any holder can determine the total amount due without external information. If the amount is vague or relies on factors outside the document itself, it fails the test set out in the Bills of Exchange Act.

Promissory notes are inherently negotiable, meaning they can be transferred from one person to another through a process called endorsement and delivery. When a lender signs the back of the note and gives it to a third party, that third party may become a holder in due course. This legal status allows the new holder to enforce the note against the borrower often without being subject to the same defenses the borrower had against the original lender.

What is a Loan Agreement

A loan agreement is a bilateral contract that involves a more extensive set of terms and conditions than a simple promissory note. While a note is primarily a promise by the borrower, a loan agreement is signed by both the lender and the borrower and outlines the mutual obligations of each party. These agreements are the standard for significant financial transactions, such as mortgages, business acquisitions, and large personal loans.

Within the structure of a loan agreement, you will typically find detailed sections covering representations and warranties. These are statements of fact that the borrower makes about their financial health and legal authority to enter into the loan. If any of these statements prove to be false, it can trigger an immediate default, giving the lender the right to demand full repayment before the original due date.

Loan agreements also include covenants, which are promises by the borrower to perform certain actions or refrain from others during the life of the loan. For instance, a business borrower might promise to maintain a certain level of insurance or not to take on additional debt without the consent of the lender. These clauses provide the lender with a high degree of control and oversight, which is not usually possible with a standard promissory note.

The default and remedies section of a loan agreement is where the lender finds their greatest protection. It defines exactly what constitutes a default, such as missing a payment, becoming insolvent, or breaching a covenant. It also outlines the specific steps the lender can take to recover their funds, including the acceleration of the debt and the right to seize any collateral that has been pledged as security for the loan.

What is an IOU

The IOU is the most informal method of documenting a debt in the country of Canada. The term itself stands for I owe you and represents a simple written acknowledgment of a liability. Unlike the other two documents, an IOU does not necessarily contain an express promise to pay the money back by a certain date. It is primarily used as a piece of evidence to prove that a debt exists between two individuals.

Because an IOU is so basic, it often lacks the essential details required for efficient legal enforcement. It may not mention an interest rate, a repayment schedule, or what happens if the borrower fails to pay. In a Canadian court, a judge would have to look at the circumstances surrounding the IOU to determine the implied terms of the loan. This can lead to unpredictable results and a more expensive legal process if the parties end up in a dispute.

An IOU is not a negotiable instrument under the federal Bills of Exchange Act. This means it cannot be easily sold or transferred to a third party in the same way a promissory note can. If a lender holds an IOU and wants someone else to collect the debt, they would generally need to follow the more complex provincial rules for the assignment of a contract. This lack of transferability makes the IOU a poor choice for any transaction with a commercial element.

Despite its limitations, an IOU is still better than no documentation at all. In small claims court, an IOU signed by the borrower is a powerful piece of evidence that can prevent the borrower from claiming the money was a gift. However, lenders should be aware that the evidentiary value of an IOU may diminish over time if they do not make a demand for payment or if they allow the provincial statute of limitations to expire.

Key Differences in One View

Enforceability and Detail

The level of detail in a document directly impacts its enforceability in the Canadian legal system. A loan agreement is at the top of the hierarchy because it leaves very little to interpretation. Every aspect of the relationship between the lender and the borrower is written down, making it much easier for a court to determine if a breach has occurred. This document is the preferred choice when the parties do not have a pre-existing relationship of high trust.

Promissory notes offer a high degree of enforceability because they are governed by specific federal legislation. The Bills of Exchange Act provides a set of ready made rules for how these notes are interpreted and enforced. If a note meets the statutory requirements, the process for obtaining a judgment in court can be much faster than for a general contract. This makes the promissory note a highly effective tool for straightforward lending where the parties want a professional and legally sound document.

Risk Exposure and Flexibility

Risk exposure varies significantly depending on the document chosen. An IOU carries the highest risk for the lender because it offers the fewest protections and the least clarity. If the borrower refuses to pay, the lender may have to spend more money on legal fees than the debt is actually worth. Loan agreements provide the most protection by allowing for the inclusion of security interests and detailed default triggers that can protect the lender before the borrower completely runs out of money.

Flexibility is a key advantage of the loan agreement. It can be tailored to fit incredibly complex scenarios, such as construction loans where funds are released in phases based on project milestones. Promissory notes are less flexible because they must follow the strict definitions of the federal Act to remain valid. If you add too many conditions or complex clauses to a promissory note, you might accidentally turn it into a simple contract, losing the benefits of negotiability and the federal statutory framework.

When a Promissory Note Is the Right Choice

A promissory note is the ideal instrument for personal loans between friends and family members in the country of Canada. It provides a formal structure that helps both parties treat the transaction with the seriousness it deserves without the overwhelming complexity of a full loan agreement. By clearly stating the principal amount and the interest rate, a promissory note helps avoid the misunderstandings that frequently lead to the breakdown of personal relationships over money.

This document is also a popular choice for small business financing, especially in the early stages of a company. When a startup receives seed funding from an angel investor, a promissory note can be used to record the debt quickly and efficiently. It allows the business to get the capital it needs without incurring high legal fees. Furthermore, these notes can sometimes be structured as convertible notes, which can be turned into equity in the business at a later date if certain conditions are met.

Short term bridge loans also benefit from the use of a promissory note. If a person needs a small amount of money for a few months to cover an emergency, the promissory note provides a legally binding record that is easy to create and sign. Because the duration of the loan is short, the parties may not need the extensive covenants and monitoring provisions found in a full loan agreement. The simplicity of the note makes it a practical solution for these temporary financial gaps.

When a Loan Agreement Makes More Sense

Large scale financial transactions in the country of Canada absolutely require a loan agreement. When hundreds of thousands or millions of dollars are at stake, the parties cannot afford any ambiguity. A loan agreement ensures that the rights of the lender are protected even in the event of the borrower's bankruptcy or other financial distress. It provides the legal foundation for the lender to recover as much of their capital as possible through structured legal processes.

Secured lending is another area where a loan agreement is essential. If a borrower is pledging their car, their home, or their business inventory as collateral, a loan agreement is used to describe that security in detail. This documentation is necessary to ensure that the lender's interest in the collateral is properly registered under provincial laws, such as the Personal Property Security Act. Without a proper loan agreement, a lender may find they have no legal right to seize the assets if the borrower stops making payments.

Complex business loans involving multiple parties or specific financial goals also demand the use of a loan agreement. For example, if a company is borrowing money to expand into a new market, the lender may want to include covenants that require the company to meet specific revenue targets. These types of arrangements require the space and the detail that only a full contract can provide. A loan agreement allows the parties to build a bespoke financial relationship that addresses the unique risks and opportunities of their specific situation.

When an IOU May Be Enough

An IOU may be sufficient for very small, informal sums of money where the lender is comfortable with a high degree of risk. If a person lends a small amount to a close friend for a few days, a simple signed note serves as a useful reminder for both parties. In these instances, the social pressure of the friendship is often a more significant motivator for repayment than the threat of legal action. The IOU simply documents the intent of the parties at the time of the transfer.

This document can also serve as a temporary record of debt in a fast moving situation. If a person borrows money and needs to provide a receipt immediately, a quick IOU can be used until a more formal document can be drafted and signed. This ensures that there is at least some written record of the transaction from the very beginning. However, it is always advisable to replace the IOU with a promissory note or a loan agreement as soon as possible to ensure that both parties are fully protected.

Finally, an IOU can be a helpful tool for tracking small business expenses or inter company debts that are expected to be settled within a short timeframe. It provides a basic audit trail that can be used by accountants to reconcile the books. While it does not offer the same level of legal protection as a formal contract, it is a practical way to manage small liabilities in a busy environment. As long as the sums involved are small and the parties have a high level of trust, the IOU can be a useful administrative tool.

Risks of Choosing the Wrong Document

Choosing the wrong document for a loan in the country of Canada can lead to severe legal and financial consequences. One of the most significant risks involves the federal Criminal Code and the laws surrounding the criminal interest rate. As of the start of the year 2025, any person who enters into an agreement to receive interest at an annual percentage rate higher than 35 percent may be committing a criminal offense. This new limit applies to the vast majority of personal and small business loans across the country.

Lenders must be extremely careful when calculating the interest on a loan. The definition of interest under the Criminal Code is very broad and includes all charges and expenses, such as fees, commissions, and penalties. If a lender uses a document that includes multiple fees that push the total cost of borrowing above the 35 percent limit, the entire interest provision may be found to be illegal. This could result in the lender being unable to collect any interest at all and could even lead to criminal charges.

Another major risk is the provincial statute of limitations. In most Canadian provinces, a lender has a limited window of time to start a lawsuit to collect a debt. In provinces like Ontario and British Columbia, this period is typically two years from the date the debt became due or the date the borrower last acknowledged the debt in writing. If a lender uses an informal document like an IOU that doesn't have a clear repayment date, they might find themselves unable to enforce the debt in court because they waited too long to take action.

In a family setting, the risk of a loan being treated as a gift is a serious concern. If a parent lends money to a child to buy a home and there is no clear documentation, a court may assume the money was a gift. This can become a major problem if the child later goes through a divorce, as the spouse may claim that the gifted money is part of the matrimonial property to be shared. A properly executed promissory note is the best way to prove that the money was a loan that was intended to be repaid.

The federal Bills of Exchange Act also imposes specific requirements for notes used in consumer transactions. Under Part V of the Act, if a promissory note is issued for a consumer purchase, it must be prominently marked with the words Consumer Note on its face. If a business lender fails to include this marking, the note may be unenforceable against the consumer. This is a common mistake made by inexperienced lenders who use generic templates that are not designed for the specific laws of the country of Canada.

Finally, there is the risk of personal liability for multiple borrowers. If a note or agreement is not drafted carefully, a lender might find they can only collect a portion of the debt from each borrower rather than the full amount from any one of them. Under the federal Act, a note that uses the phrase I promise to pay and is signed by multiple people creates joint and several liability. This is a vital protection for lenders that can be lost if the document uses different or less precise language.

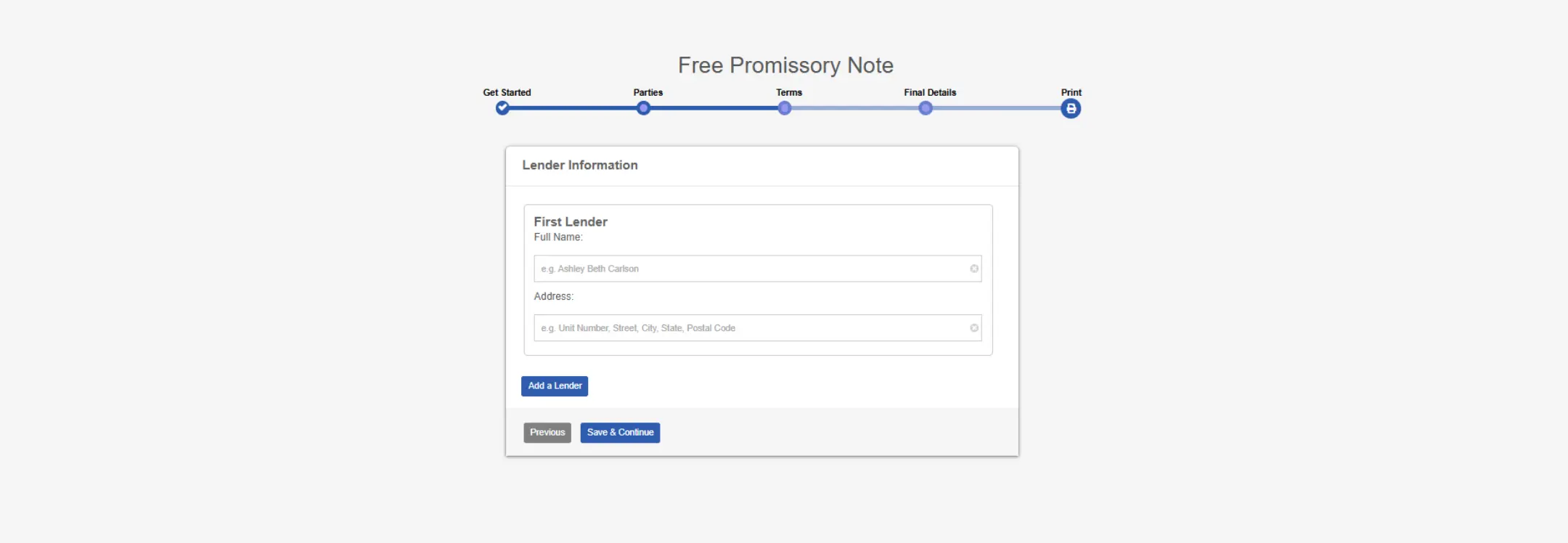

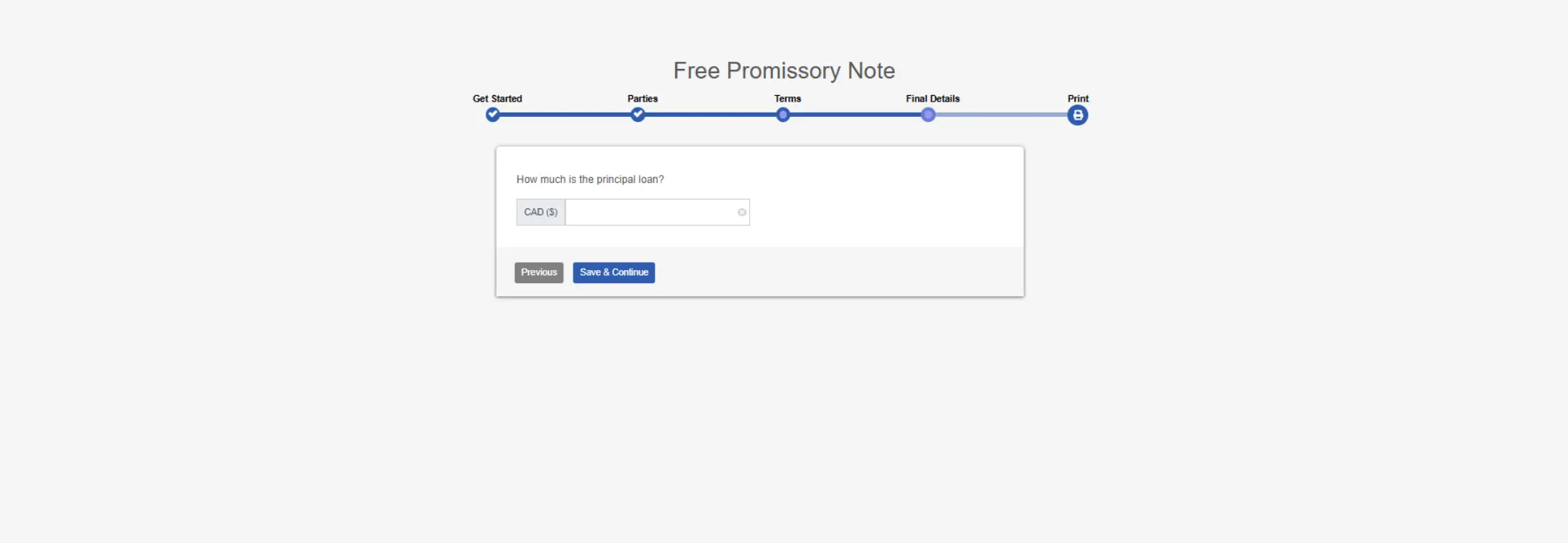

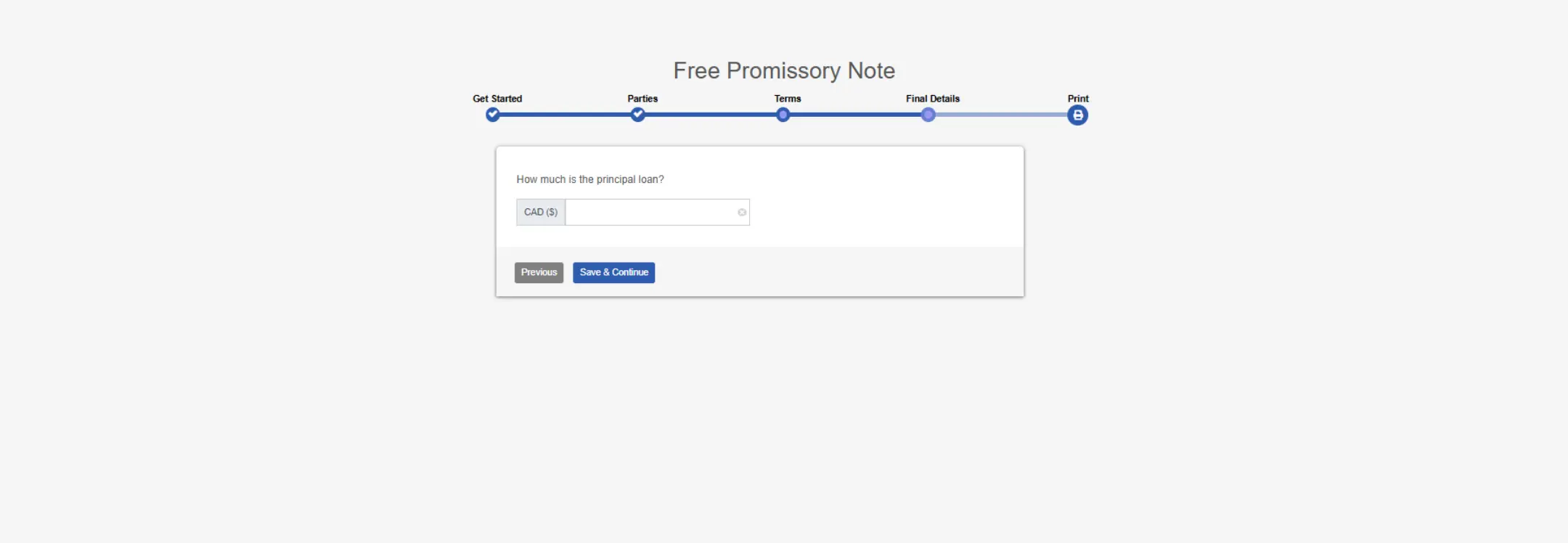

How to Create a Promissory Note with Ziji Legal Forms

1. Choose template

Select the Canadian version of the Promissory Note template that fits your specific lending needs.

2. Add Parties' Details

Enter the full legal names and the current mailing addresses for every person involved in the transaction.

3. Add Term Details

Input the principal amount and the interest rate while ensuring it does not exceed the legal limit.

4. Add Final Details

Include the repayment dates and determine if you want to include any collateral or late fee provisions.

5. Preview and print.

Check the final document for any errors and then print it for all parties to sign.

Conclusion: Choose the Level of Structure Your Loan Deserves

The decision to use a promissory note, a loan agreement, or an IOU depends on the level of risk and the complexity of your financial transaction. Promissory notes offer a balanced approach with strong federal legal backing, while loan agreements provide the most comprehensive protection for significant sums. Lenders must always be aware of the 35 percent criminal interest rate limit and provincial limitation periods to ensure their documents remain enforceable in a Canadian court. By taking the time to select the correct instrument, you protect your capital and maintain the clarity of your financial relationships. A well documented loan is the best way to prevent future legal disputes and ensure a successful repayment.

Promissory Note FAQs

What else can a promissory note be called?

A promissory note can also be referred to as follows: demand note, IOU “I owe you”, loan agreement, or promise to pay agreement.

What is a promissory note?

A promissory note is a legal document where the borrower promises to repay the loan to the lender under the terms and conditions listed in the note.

What points should the promissory note cover?

You can create a promissory note using our simple template. A promissory note should have the terms as follows:

Governing law: Select the province where the lender resides and the promissory note will be customized for that jurisdiction.

Parties’ Info: Lender and borrower information such as full name and addresses.

Loan amount: How much is the loan.

Collateral: What security will be seized by the lender if the borrower fails to repay the loan. Describe the item in detail to ensure the collateral is not ambiguous. (e.g. list the VIN number if it is a vehicle, or a serial number if it is electronics)

Interest payment: How much interest is being charged to the loan, if applicable

Repayment schedule: How will the loan be paid back, whether in equal payments, a lump sum, or on demand. Payment schedules are flexible and can be made weekly, monthly, quarterly, semi-quarterly, and annually.

Prepayment penalty: List the penalty for repaying the loan early, if applicable.

Late penalty: How much additional interest will be charged if the payment is late, if applicable.

Do you need to notarize a promissory note?

Only the signature of the borrower and the lender are required to have a valid and enforceable promissory note. But if the loan is a substantial amount, it may be prudent to have it notarized since it adds a layer of authenticity if there are any future disputes regarding the loan.

What jurisdictions can use our promissory note?

You can use our template to create a legal and valid promissory note for the following jurisdictions:

Alberta

British Columbia

Manitoba

New Brunswick

Newfoundland and Labrador

Northwest Territories

Nova Scotia

Nunavat

Prince Edward Island

Saskatchewan

Yukon

AB

BC

MB

NB

NL

NT

NS

NU

PE

SK

YT

Author

Mandar Sonavane

|

Legal Content Writer at Ziji Legal Forms Inc.

Symbiosis International University

Mandar is a legal content writer specializing in the development of clear, practical, and easy-to-understand legal resources. With a strong focus on legal research, content creation, and plain-language writing, he works closely with our legal professionals to ensure that legal documents and educational materials are accurate, accessible, and user-friendly. At Ziji Legal Forms Inc., Mandar is responsible for researching legal topics, drafting and reviewing content, and helping transform complex legal concepts into straightforward guidance that empowers individuals and businesses to confidently navigate their legal needs.

Reviewed By

Histon Shek

|

General Counsel and Co-Founder at Ziji Legal Forms Inc.

University of Alberta

Histon Shek was called to the Alberta Bar in 2006. He holds a BA in Sociology and Philosophy and an LLB from the University of Alberta. As co-founder of Ziji Legal Forms Inc., he focuses on making legal documents accessible and affordable, overseeing legal integrity and content development.