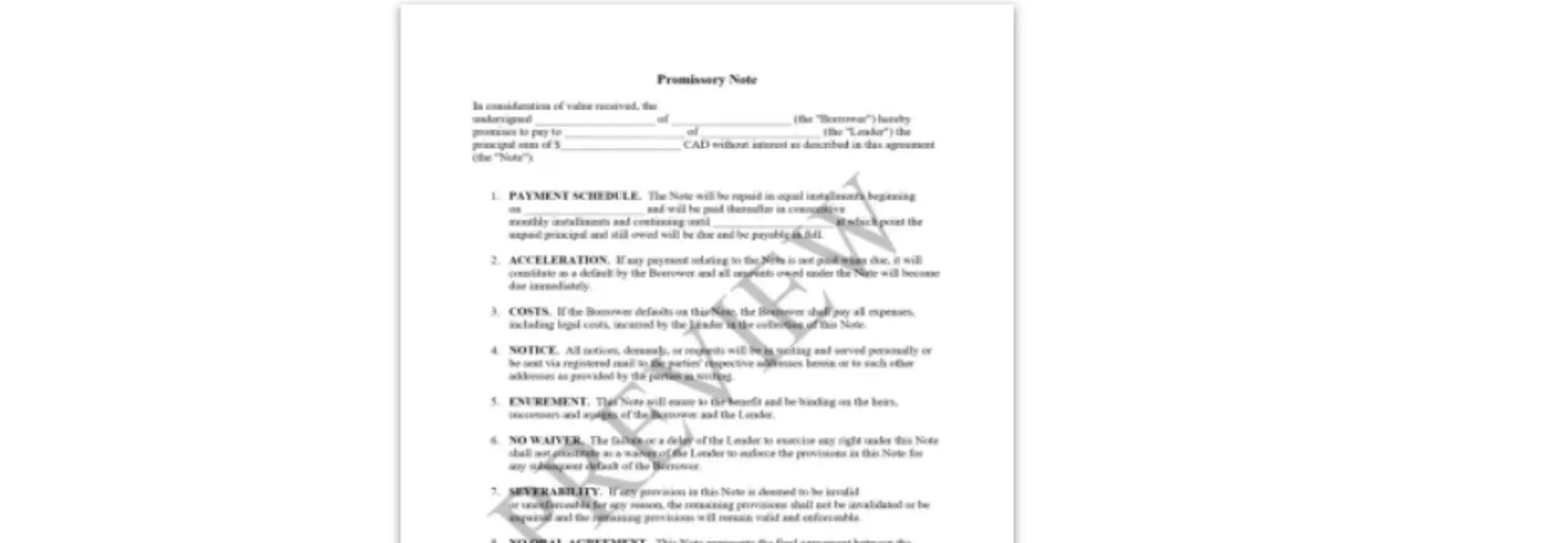

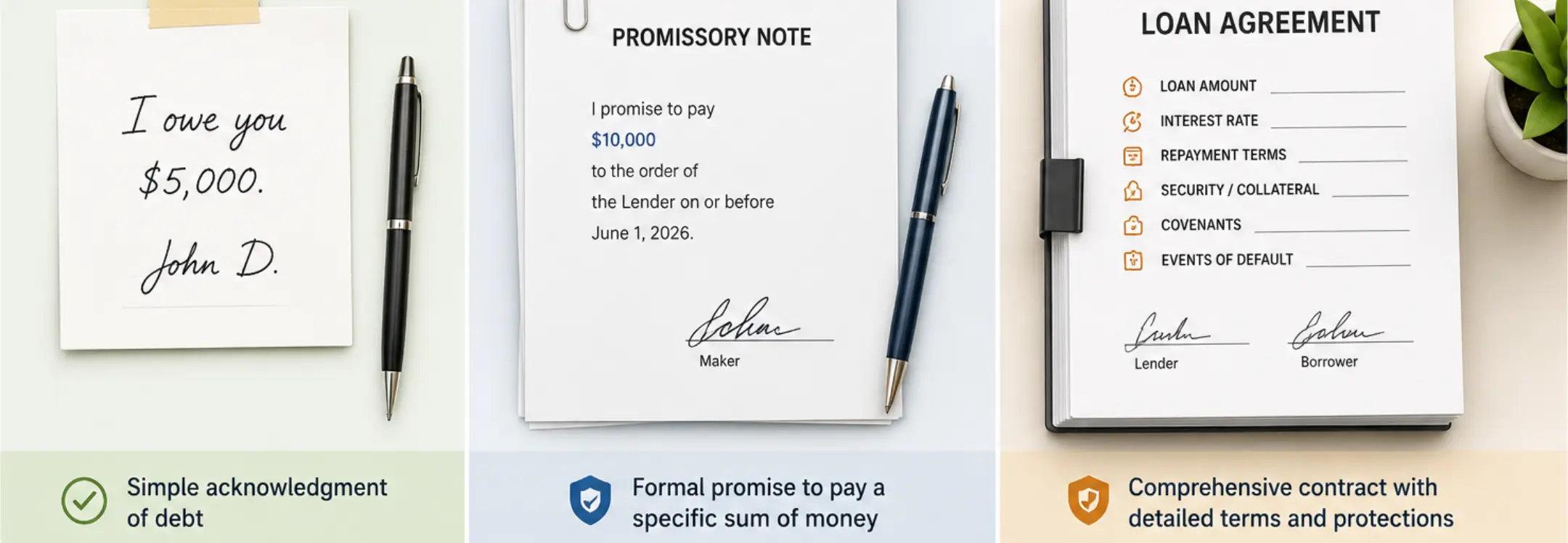

- A promissory note is a legal document where a borrower makes an unconditional promise to repay a specific sum to a lender.

- In Canada, these instruments are governed by the federal Bills of Exchange Act, ensuring consistency across all provinces.

- Effective January 1, 2025, the criminal interest rate in Canada is capped at 35 percent Annual Percentage Rate for most loans.

- Section 4 of the Interest Act requires any interest rate to be expressed as an annual percentage, or it is legally capped at 5 percent.

- Notes can be secured by collateral or unsecured, and they can be payable on a specific date or on demand.

- Proper documentation is essential for enforcement through expedited legal processes like summary judgment in provincial courts.

- You can create a Promissory Note easily using Ziji Legal Forms

Introduction: The Simplicity and Power of a Promissory Note

The financial landscape in Canada often requires a balance between informal trust and formal legal protection. Whether you are lending money to a family member for a first home or providing a short term bridge loan for a business partner, the promissory note serves as a critical bridge. It is often described as the simplest representation of a debt. It provides a clear, written record of an obligation without the overwhelming complexity of a multi-page loan agreement. This simplicity is its greatest power, as it allows individuals and small businesses to formalize debts quickly while maintaining a high degree of legal enforceability under federal law.

Despite its concise nature, a promissory note carries significant weight in the Canadian judicial system. It is not merely an IOU or a simple acknowledgment that a debt exists. Instead, it is a negotiable instrument that falls under the jurisdiction of the federal government. This means that the fundamental rules governing its validity are the same whether the note is signed in Toronto, Vancouver, or Halifax. By putting a promise in writing, both parties move away from the ambiguity of verbal agreements, which are notoriously difficult to prove in court. A well-drafted note ensures that the terms of repayment are transparent and that the lender has a clear path to recovery if a default occurs.

How a Promissory Note Works

The Basic Process

The process begins when two parties agree on the terms of a loan, including the amount, the interest, and the timeline for repayment. The lender then prepares the document, which acts as the official evidence of the debt incurred by the borrower. Unlike many other contracts, the most vital part of the process is the signature of the maker, who is the person borrowing the money. Once the borrower signs the note, they have made an unconditional promise to pay. The lender typically keeps the original document as security, providing it back to the borrower only after the final payment has been made and the debt is satisfied.

In the modern Canadian context, the exchange of funds often follows the execution of the note immediately. The note creates a transparent record that protects the interests of both sides. For the lender, it serves as a financial asset that can, in many cases, be transferred or sold to a third party. For the borrower, it defines the exact limits of their liability, ensuring that the lender cannot unilaterally change the interest rate or demand early repayment unless such terms were explicitly agreed upon in writing. This structured flow of capital is essential for maintaining healthy financial relationships and ensuring that private lending remains a viable option for those who may not seek traditional bank financing.

Legal Standing and Enforcement

Promissory notes in Canada hold a unique legal status because they are governed by the federal Bills of Exchange Act. This statute defines a note as an unconditional promise in writing made by one person to another, signed by the maker, engaging to pay a sum certain in money. Because the promise is unconditional, the legal system treats these documents with a high degree of respect. If a borrower defaults, the lender does not necessarily have to go through a full, lengthy trial to recover their funds. In many provinces, lenders can apply for a summary judgment or a summary trial.

A summary judgment is an expedited process where a judge decides the case based on written evidence rather than live testimony. If the note is clearly drafted and the signature is authentic, the court can grant a judgment in the lender's favor relatively quickly. This efficiency makes the promissory note a much more powerful tool than a standard contract for debt collection. Furthermore, the rule of contra proferentem applies to these documents in Canada. This means that if there is any ambiguity or lack of clarity in the text, the courts will generally interpret the terms in favor of the person who did not draft the document, which is usually the borrower.

Types of Promissory Notes

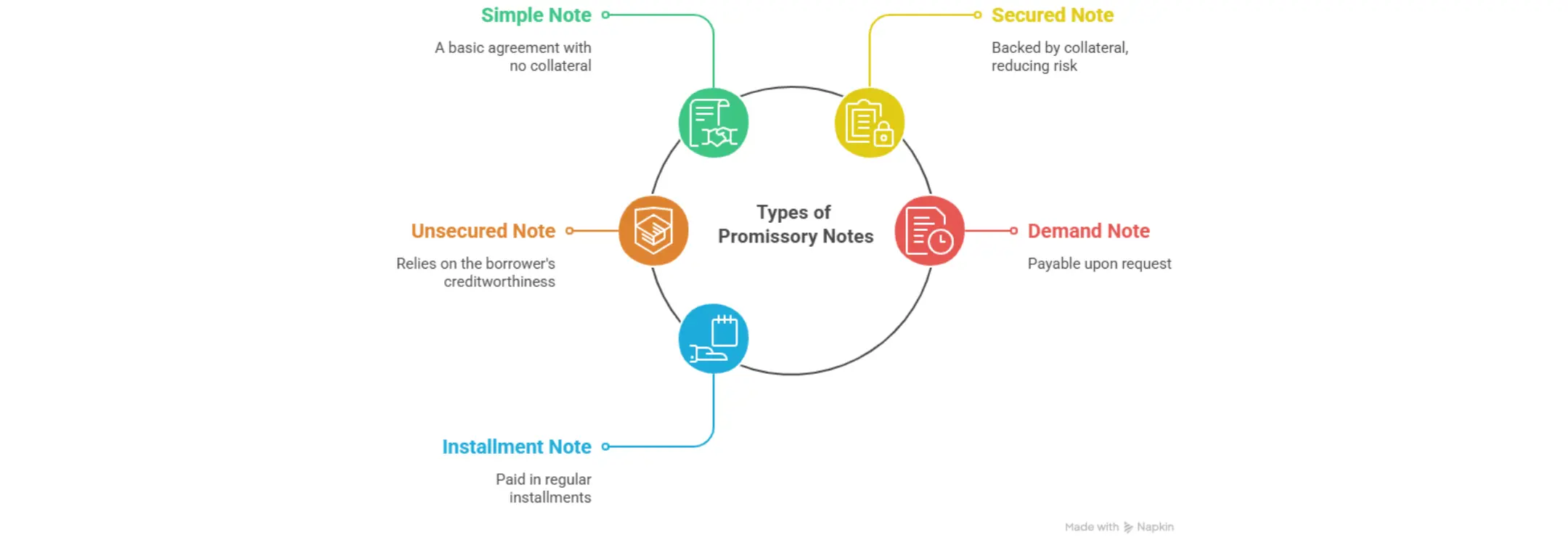

Simple or Personal Promissory Note

A simple promissory note is most frequently used for straightforward loans between individuals who have an established relationship of trust. This might include loans between friends or family members where the repayment is expected in a single lump sum by a specific date. These notes are usually shorter and contain only the most essential information, such as the names of the parties, the amount borrowed, and the due date. While they may or may not include interest, they still provide the lender with a legally binding document that can be used in court if the relationship sours and the money is not returned as promised.

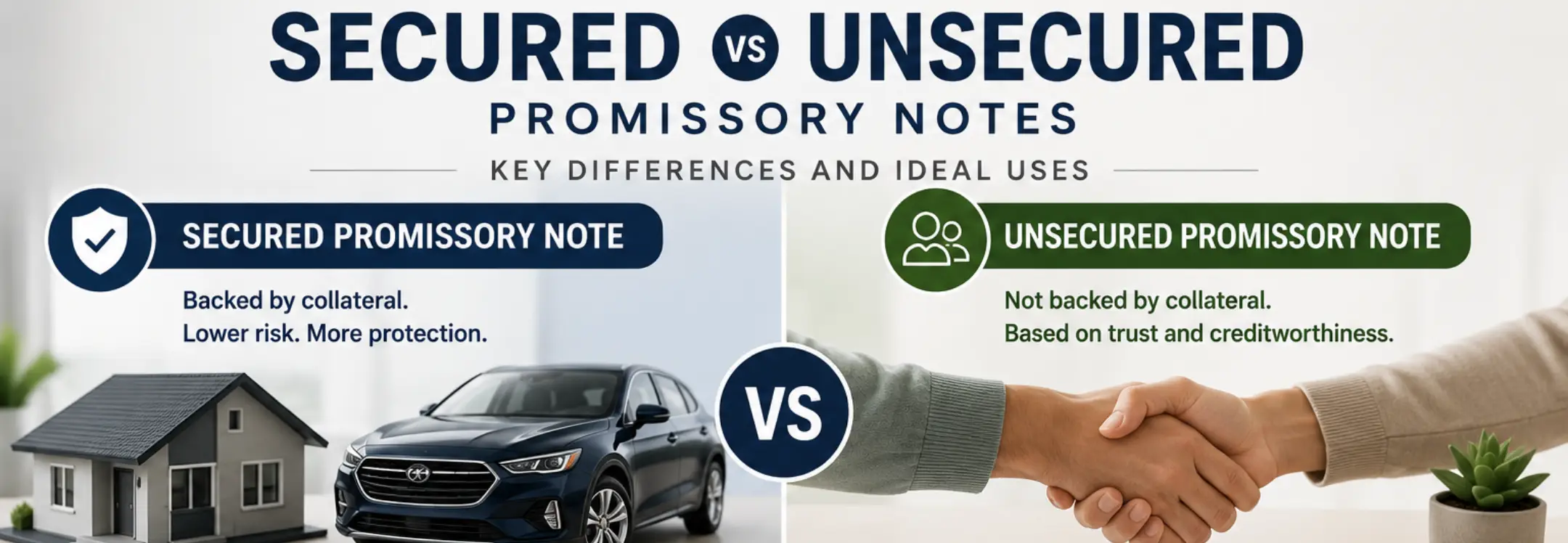

Secured Promissory Note

A secured promissory note provides an extra layer of protection for the lender by linking the debt to a specific asset or collateral. In Canada, this collateral could be a vehicle, equipment, or even real estate. If the borrower fails to meet their repayment obligations, the lender has the legal right to seize and sell the collateral to satisfy the debt. This structure is common in small business lending and for larger personal loans where the lender wants more than just a promise to pay. To be fully effective, a secured note is often accompanied by a security agreement and registered under provincial personal property registries.

Unsecured Promissory Note

An unsecured promissory note is based entirely on the borrower's creditworthiness and their personal promise to repay the funds. There is no collateral attached to the note, meaning the lender has no direct claim to any of the borrower's assets if a default occurs. Because the risk to the lender is higher, these notes often carry higher interest rates than secured ones. If the borrower defaults, the lender's only recourse is to initiate a lawsuit to obtain a court judgment, which they can then use to garnish wages or seize assets through the provincial sheriff's office. These are typical for small, informal loans where the borrower has a strong reputation.

Demand Note

A demand note is unique because it does not have a fixed maturity date or a set schedule for repayment. Instead, the entire balance becomes due and payable whenever the lender makes a formal request for the money. These are highly flexible and are often used for shareholder loans to a corporation or loans between family members where the lender wants the ability to call in the debt if their own financial circumstances change. Under Canadian law, if a note does not specify a repayment date, it is legally treated as a demand note, meaning it is payable as soon as the lender asks for it.

Installment Note

An installment note is the most common type for structured loans, requiring the borrower to make regular payments over a set period. These payments usually happen monthly and include both a portion of the principal amount and the accrued interest. This format is ideal for borrowers who cannot afford to pay back a large sum all at once, as it allows them to budget for a predictable repayment timeline. Most installment notes in Canada include an acceleration clause, which states that if the borrower misses a single payment, the lender can declare the entire remaining balance due immediately, rather than waiting for each individual installment date.

Key Elements Every Promissory Note Should Include

Principal Amount

The principal amount is the exact sum of money that is being lent to the borrower. In a Canadian promissory note, it is standard practice to write this amount in both figures and words to prevent any confusion or unauthorized changes to the document. For example, a loan might be listed as ten thousand dollars ($10,000). The currency should also be clearly specified as Canadian dollars to avoid any disputes if the parties cross borders or deal with international accounts. The principal is the foundation of the note and the base upon which all interest calculations are made throughout the life of the loan.

Interest Rate and Usury Compliance

Canada has strict laws governing how much interest a lender can charge. As of January 1, 2025, the criminal rate of interest was reduced from an effective annual rate of 60 percent to an annual percentage rate of 35 percent. Charging more than this limit is a criminal offense under the Criminal Code of Canada. Additionally, the federal Interest Act requires that the interest rate be expressed as an annual rate. If you only list a monthly or weekly rate without stating the annual equivalent, the law may cap the interest you can collect at just 5 percent per year, regardless of what you originally agreed upon with the borrower.

Repayment Schedule and Terms

The repayment terms outline exactly how and when the lender will get their money back. This section must be specific to be enforceable. It should state whether the payments are lump sum, installments, or on demand. For installment notes, you must list the frequency of payments, such as monthly or bi-weekly, and the specific date each payment is due. It is also important to specify the method of payment, such as electronic transfer, cheque, or bank draft. Clear repayment terms prevent misunderstandings and ensure that the borrower knows their exact obligations every month, which helps maintain a positive relationship between the parties.

Maturity Date

The maturity date is the final deadline by which the entire balance of the loan, including all principal and interest, must be fully repaid. For term notes, this is a specific calendar date. Having a clear maturity date is essential for both parties because it sets a definitive end to the financial arrangement. For lenders, it provides a date after which they can take legal action if the funds have not been returned. For borrowers, it provides a goal for their financial planning. If a note is a demand note, it will not have a maturity date, as the deadline is created only when the lender demands payment.

Default and Late Payment Provisions

A well-written note must anticipate the possibility that things might not go according to plan. The default provisions explain what happens if the borrower misses a payment or fails to follow other terms of the agreement. Common consequences include late fees, which must be reasonable, and a default interest rate that is higher than the standard rate but still within legal limits. Most importantly, Canadian notes should include an acceleration clause. This allows the lender to demand the full amount of the loan immediately upon a default, which is a vital protection that saves the lender from having to sue for every individual missed payment.

Security and Collateral Descriptions

If the promissory note is secured, it must contain a detailed and accurate description of the collateral. This could be the vehicle identification number for a car or the legal description of a piece of property. If the description is vague or inaccurate, the lender may find it impossible to seize the asset if the borrower defaults. In Canada, simply listing the collateral in the note is often not enough to protect the lender against other creditors. The lender should also ensure that their interest is properly registered under the relevant provincial security acts to maintain their priority and their right to the asset.

Signature Requirements

For a promissory note to be legally binding in Canada, it must be signed by the borrower. The Bills of Exchange Act explicitly requires the maker to sign the instrument to engage their liability. While the lender's signature is often included, it is the borrower's signature that creates the unconditional promise to pay. Although not always strictly required by law, it is a best practice in Canada to have the signing witnessed by an independent third party or a notary public. This provides an extra layer of protection by making it much harder for a borrower to later claim that the signature was forged or that they signed under duress.

Governing Law Clause

A governing law clause specifies which province's laws will be used to interpret and enforce the promissory note. This is particularly important in Canada because while the Bills of Exchange Act is federal, the procedures for court actions and the limitation periods for suing are provincial. For example, a note governed by the laws of Ontario might have different enforcement timelines than one governed by the laws of Alberta. By choosing a specific jurisdiction, both parties have more certainty about how a dispute would be handled and where they would need to go to court if the terms of the note are not met.

Why You Need a Written Promissory Note

Benefits for Lenders

For a lender, a written promissory note is the most essential tool for protecting their investment. It provides concrete evidence of the loan, making it much easier to prove in court than a verbal agreement. The note clearly defines the interest rate and the repayment schedule, ensuring that the lender receives the full return they expect. Furthermore, the ability to use expedited court processes like summary judgment can save a lender thousands of dollars in legal fees if they ever need to sue for recovery. A note also allows a lender to secure the loan with collateral, which significantly reduces the risk of a total financial loss.

Benefits for Borrowers

Borrowers also benefit from a written note because it provides them with a clear and definitive record of their obligations. It protects them from a lender who might otherwise try to change the terms of the loan or demand payment earlier than agreed. A promissory note can also be a useful document for a borrower's own records, helping them track their debts for tax or accounting purposes. In some cases, having a formalized note can even help a borrower build a positive financial history if the lender is willing to provide a letter of reference or confirm that the payments were made on time according to the written schedule.

Mutual Benefits

A promissory note provides mutual benefits by establishing a foundation of transparency and trust between the parties. By putting everything in writing, both sides are forced to think through the specifics of the loan before any money changes hands, which helps prevent future misunderstandings and disputes. This clarity is especially important for loans between friends and family members, as it helps preserve personal relationships by treating the loan as a professional financial transaction. Having a clear record of the agreement ensures that both the lender and the borrower are on the same page from the beginning, which is the best way to ensure the loan is successful.

Common Mistakes to Avoid

Incomplete Payment Information

One of the most frequent errors in Canadian promissory notes is failing to be specific about how and when payments should be made. If a note simply says the money will be repaid soon or as soon as possible, it may be found to be legally unenforceable because the terms are too vague. Lenders should always include exact dates, the amount of each payment, and the specific method of delivery. Without this information, a borrower can easily delay payments without being in technical default, leaving the lender with no clear path to demand the funds or start a legal action to recover the debt.

Inadequate Default Provisions

Failing to include a clear acceleration clause is a significant mistake that can make debt collection much more difficult for a lender. Without this clause, if a borrower misses a monthly payment, the lender might only be able to sue for that specific missed payment rather than the entire balance of the loan. This can result in the lender having to file multiple, expensive lawsuits over several months or years. A strong default section should also clearly define what constitutes a default beyond just missing a payment, such as the borrower filing for bankruptcy or failing to maintain insurance on the collateral that secures the loan.

Signature and Documentation Problems

A promissory note is only as good as its execution. A common mistake is failing to ensure that the borrower's signature is properly witnessed or notarized. If a borrower later denies that they signed the document, the lender may face a difficult and expensive battle to prove its authenticity in court. Additionally, many people make the mistake of making informal, handwritten changes to a note after it has been signed. In Canada, any changes to a note should be made through a formal written amendment that is signed by both parties to ensure that the modifications are legally valid and do not invalidate the original agreement.

Interest Rate and Legal Compliance Errors

Many private lenders in Canada accidentally violate the Interest Act or the Criminal Code. A common error is charging a monthly interest rate without also stating the equivalent annual rate. As mentioned, this can result in the interest being limited to just 5 percent by a court. Another mistake is including fees or penalties that, when combined with the interest rate, exceed the 35 percent annual percentage rate limit set by the Criminal Code. Lenders must be hyper-vigilant about these calculations, as a violation of these federal laws can not only make the interest unenforceable but can also lead to criminal charges in extreme cases.

Unclear Terms and Conditions

Vague language is the enemy of an enforceable legal document. Using terms like reasonable interest or fair market value without defining how those numbers are calculated can lead to expensive disputes and potential loss of the debt. Because of the rule of contra proferentem, any confusion in the text is usually decided against the lender who drafted the note. To avoid this, parties should use clear, plain language and avoid complex legal jargon that they do not fully understand. Using a professional template is often the best way to ensure that the terminology used is legally recognized and that the terms are specific and clear.